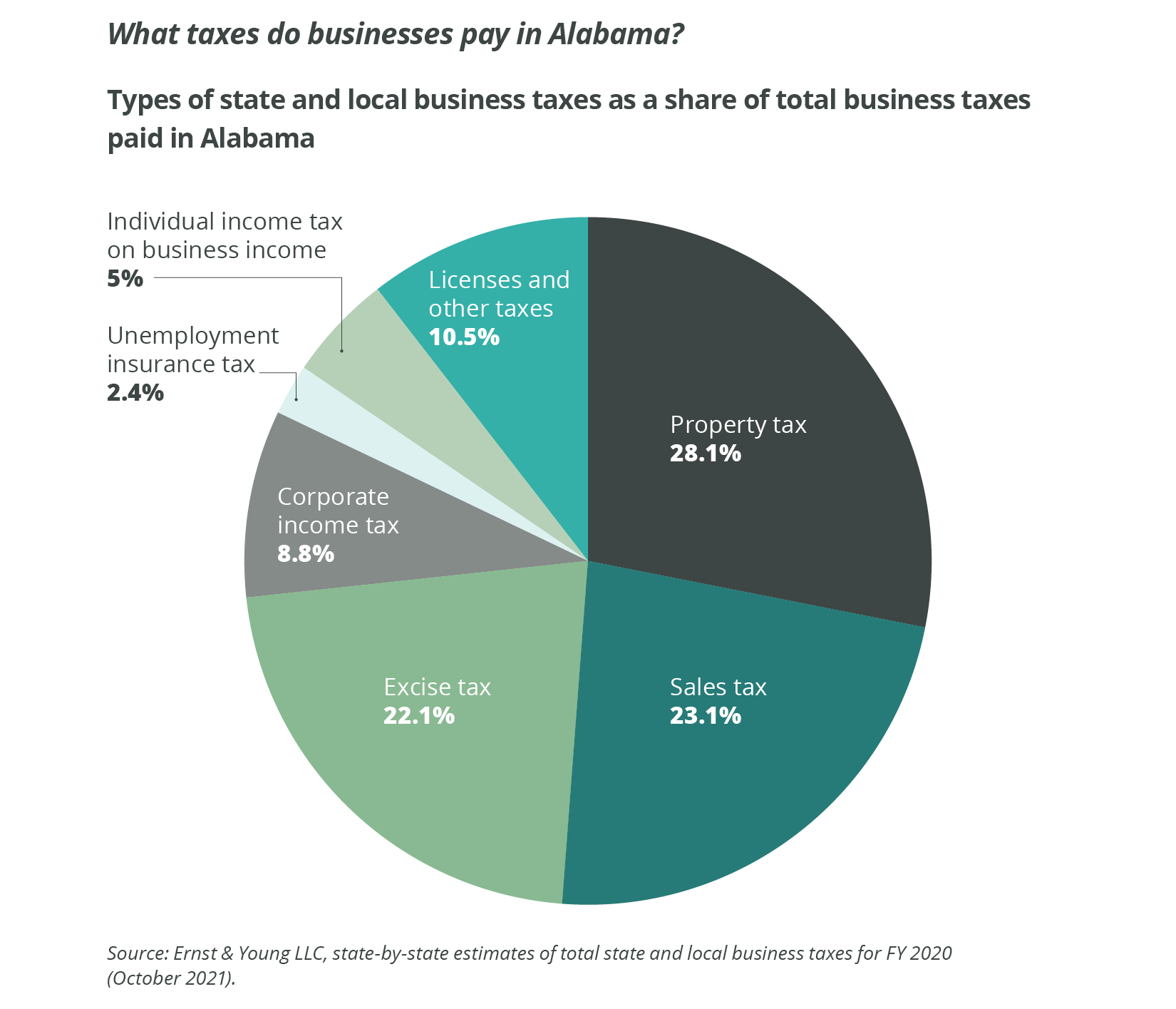

How do Alabama’s property taxes work?

The 1901 Alabama constitution established a property tax of 6.5 mills to help fund the state government. That was 30 years before our state had income or sales taxes. More than a century later, the state property tax rate has not changed.

Property tax is applied to real estate, motor vehicles and boats as a millage rate. A mill is 1/10 of a cent, so a 1-mill tax amounts to $1 of tax per $1,000 of taxable property value. Three mills of the revenue from Alabama’s 6.5-mill state property tax is earmarked for the Public School Fund, which helps pay for school construction projects, while the rest supports other services.

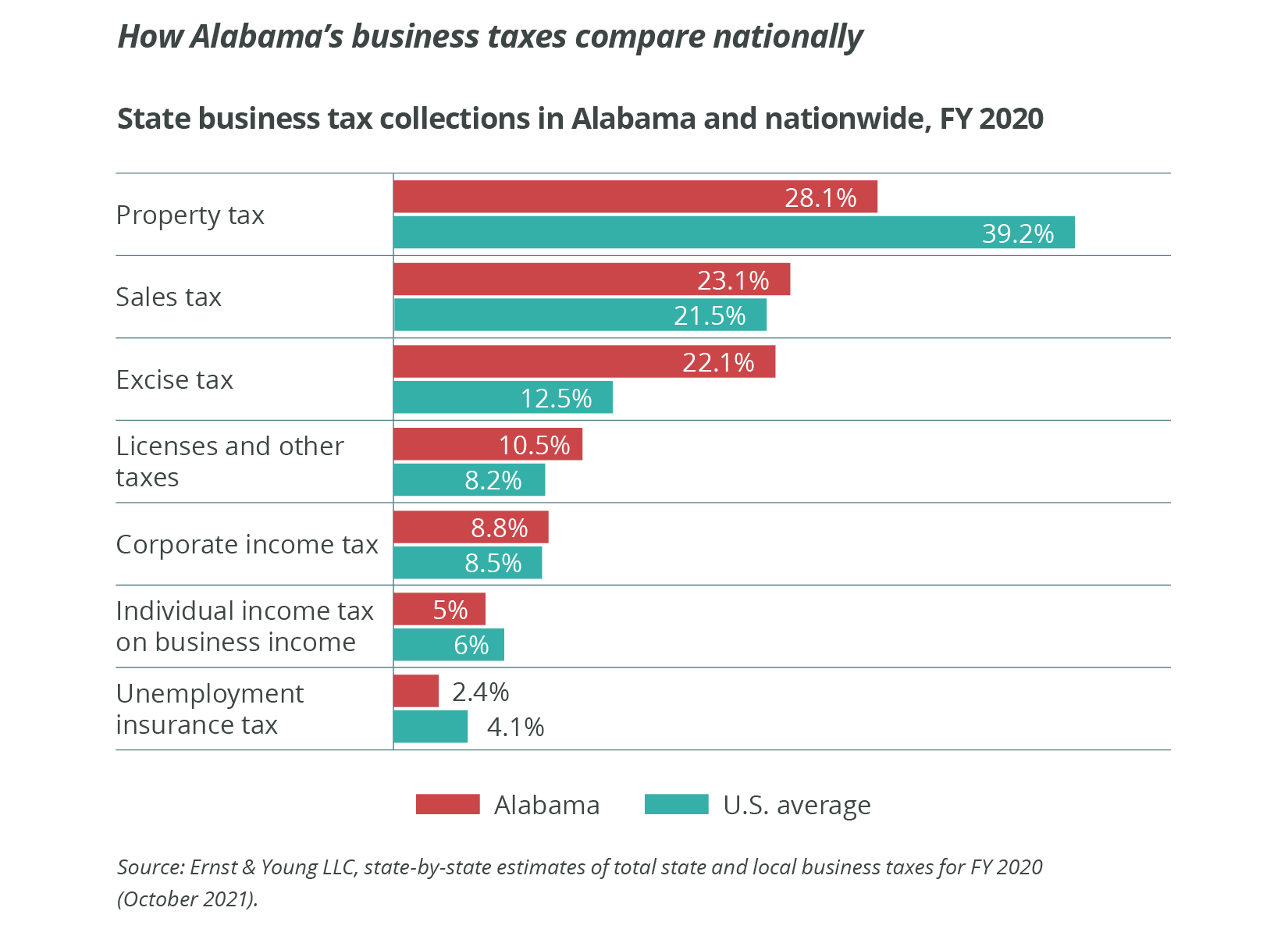

The 6.5-mill state property tax is a small part of your property tax bill. The larger part is your local property tax, which pays for public schools and local services like parks and fire protection. In 2020, local property taxes generated nearly 86% of total property tax revenues in Alabama. By state law, each school district must have at least 10 mills of local tax dedicated to education. Local property taxes (excluding the state one) vary widely depending on where you live, ranging from 19.5 mills in rural Coosa County to 109 mills in Mountain Brook (in Jefferson County). Even so, Alabama’s average local property taxes are the lowest in the country.

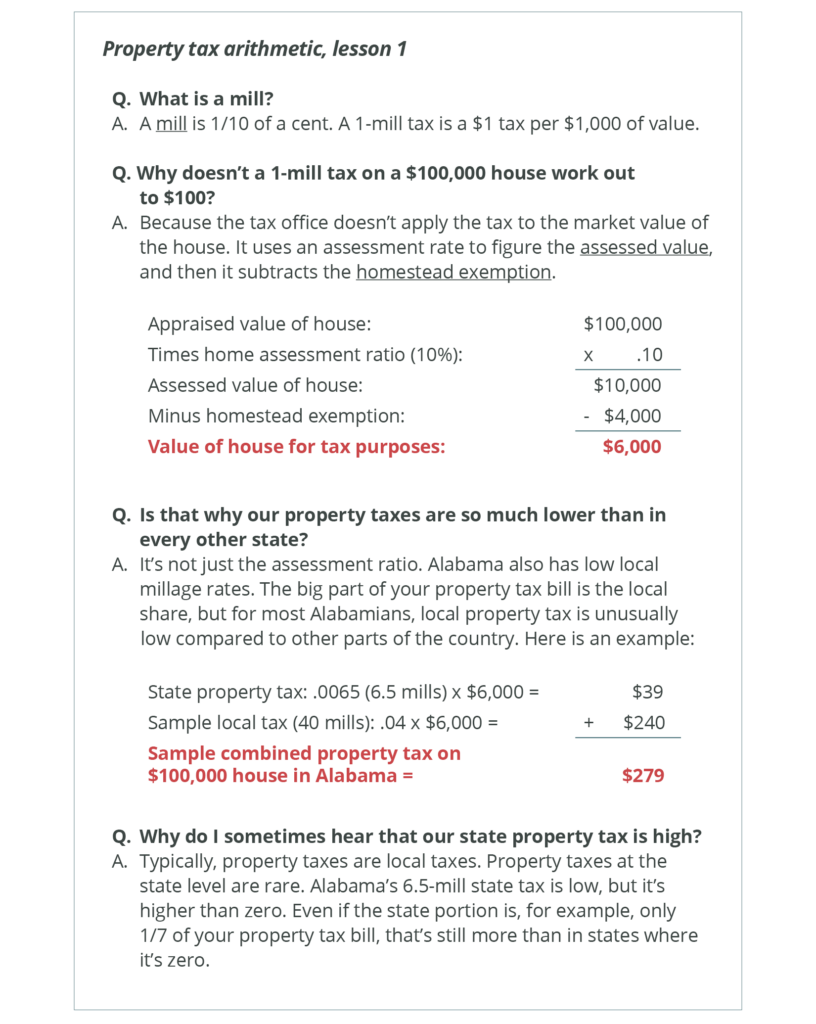

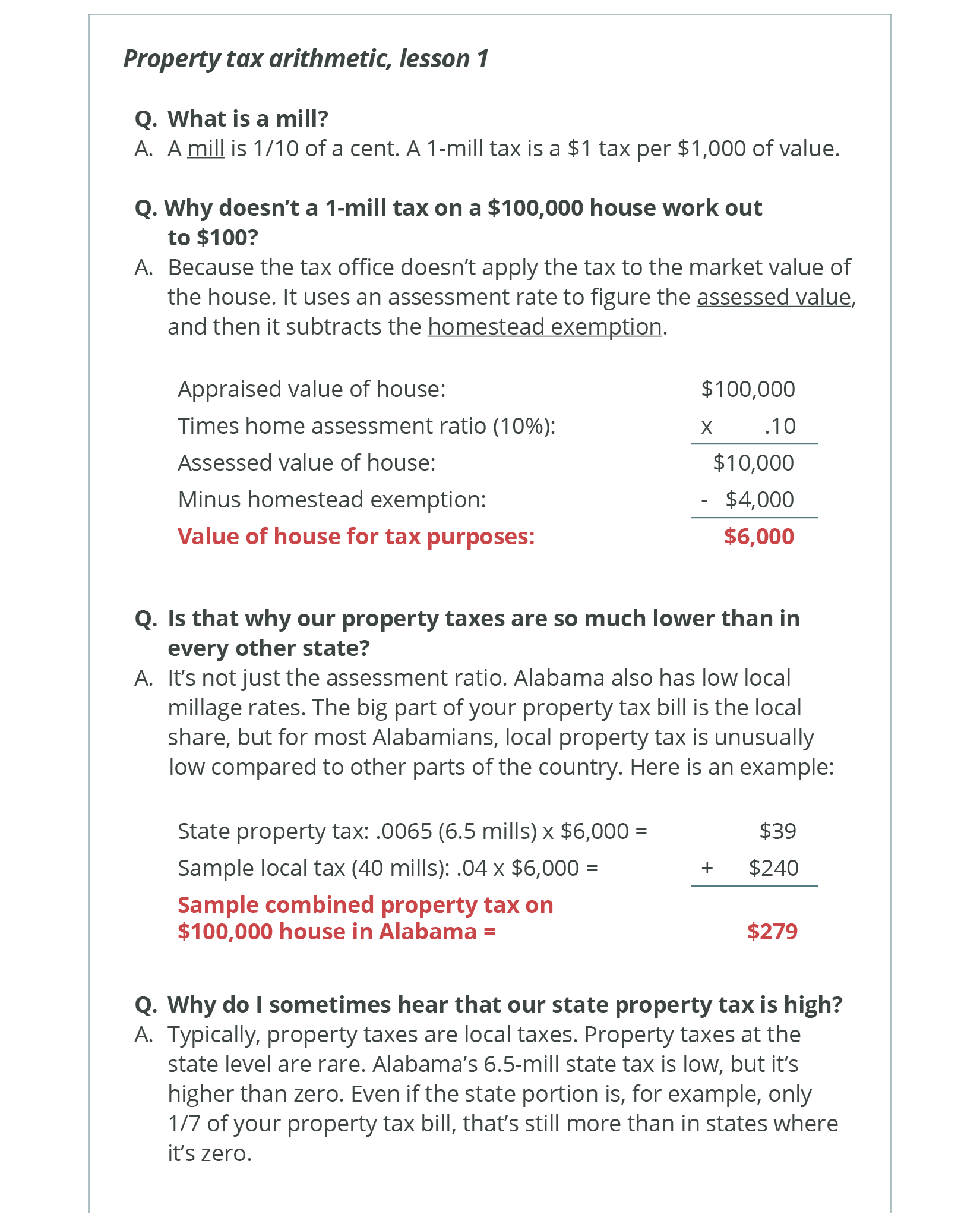

Local governments regularly assess the value of property for both state and local tax purposes. The assessed value is the portion of the appraised value (or fair market value) that the government uses to calculate the amount of property tax. (See the graphic above.)

Alabama taxes property at only a fraction of its value. Since the so-called Lid Bill capped property tax collections in 1978, the state has used the following system of property classifications for assessing taxes:

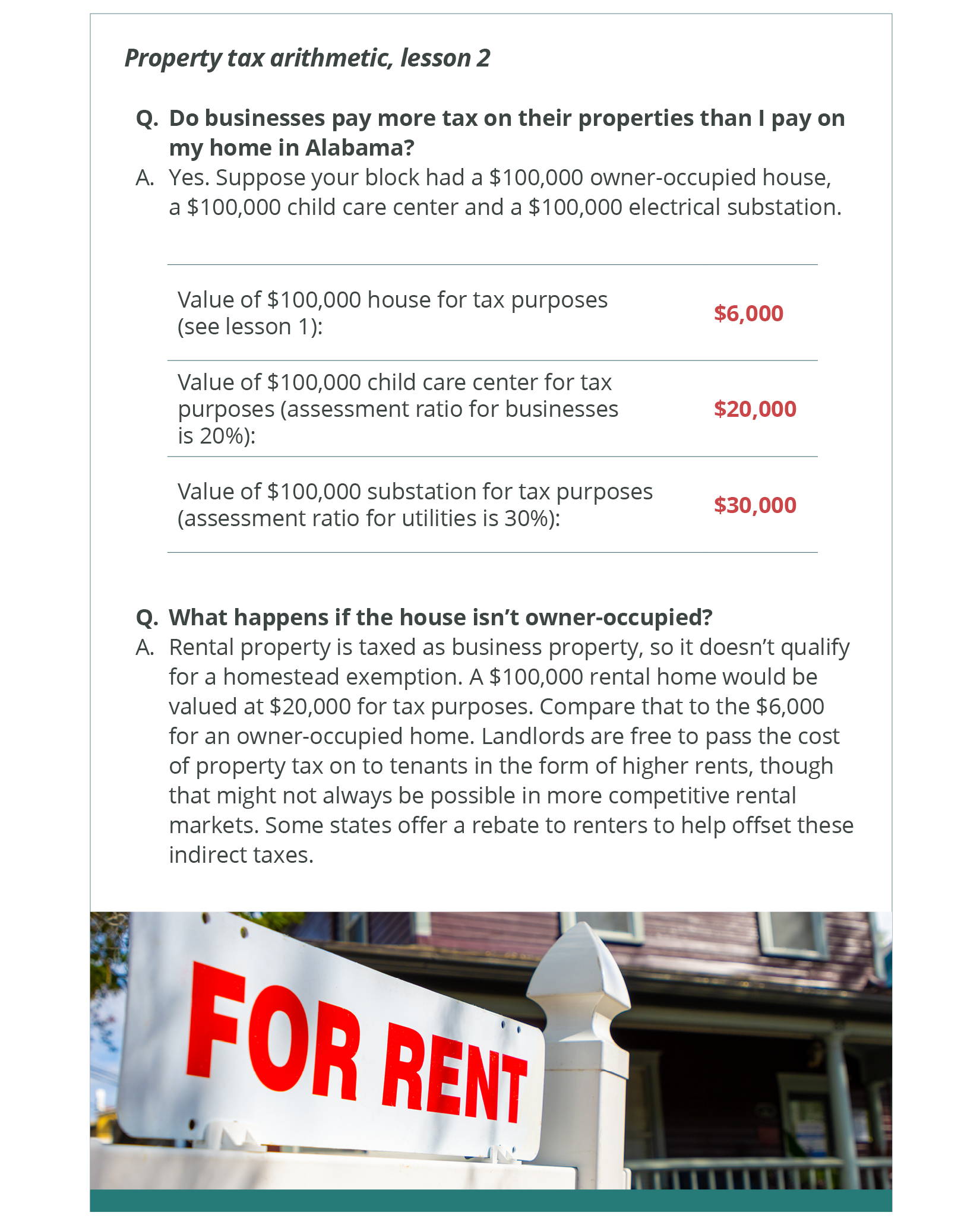

- Utility company property is assessed at 30% of fair market value.

- Commercial property is assessed at 20%.

- Individually owned vehicles are assessed at 15%.

- Farms, timberland and owner-occupied residential property are assessed at 10%. Huge corporate farms and timber holdings are treated the same as 100-acre family farms. The homestead exemption exempts from property taxes (except countywide school taxes and school district taxes) the first $4,000 of an owner-occupied home’s assessed value (an amount equal to $40,000 of appraised, actual value).

If Alabama taxed residences at their full value, a 1-mill tax on a $100,000 house would be $100. But the state taxes homes on only 10% of their value, so a $100,000 home is assessed at a taxable value of $10,000. (See the “lesson 1” graphic at the top of this page.) The homestead exemption lowers the tax even further, meaning you don’t pay on the first $4,000 of the amount subject to tax.

Alabama has numerous property tax exemptions for older adults and people who are blind or disabled. In fact, some Alabamians who are aged 65 and older or who have disabilities pay no property tax at all. Senior married couples who have a gross income of less than $12,000 are exempt from all state and county property taxes on their homestead and up to 160 acres of land. Alabamians who are blind or permanently disabled are exempt from all property taxes.

Racial inequity at a glance

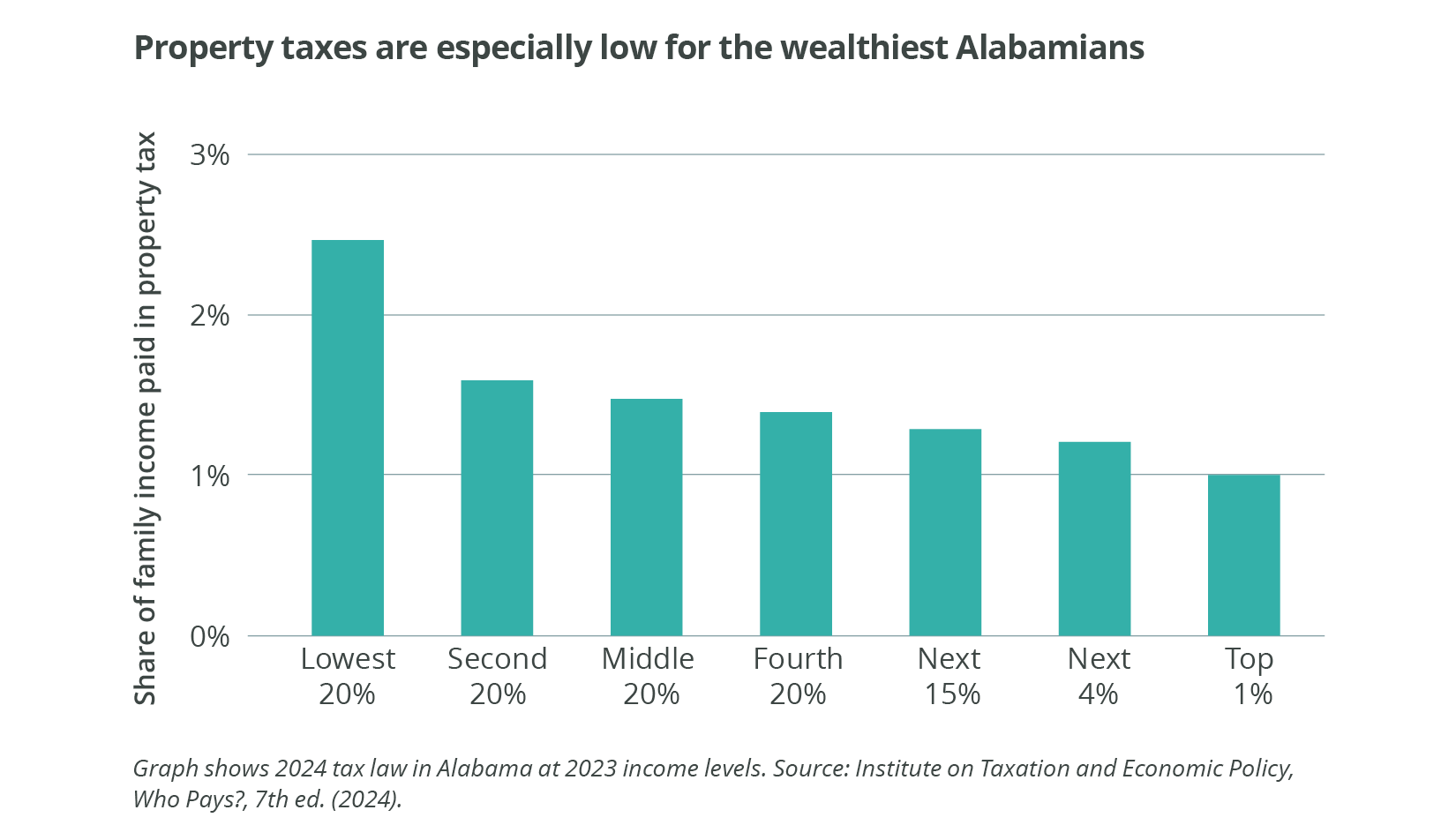

The racial impact of property taxes is complex. The most important source of household wealth for most people is homeownership. In part because of low property tax rates, Alabama’s Black homeownership rate is the nation’s fifth highest at 50.1% of households. This promotes higher rates of household and intergenerational wealth. But racial disparities in both tax assessment and property valuations reduce the benefits of a high homeownership rate.

Several counties in Alabama’s Black Belt, a region with high poverty rates and a predominantly Black population, have property tax valuations well above the average for all Alabama counties. And because Alabama earmarks most property taxes for education, Black families are disproportionately harmed by underfunded schools. Many rural Black Belt counties lack a strong economic and retail base, limiting sales taxes and other revenues for education. Coupled with constitutional restrictions on property tax rates, this forces many counties to increase home assessments to fund their schools.

Several counties in Alabama’s Black Belt, a region with high poverty rates and a predominantly Black population, have property tax valuations well above the average for all Alabama counties. And because Alabama earmarks most property taxes for education, Black families are disproportionately harmed by underfunded schools. Many rural Black Belt counties lack a strong economic and retail base, limiting sales taxes and other revenues for education. Coupled with constitutional restrictions on property tax rates, this forces many counties to increase home assessments to fund their schools.

Alabama needs to find a solution that supports homeownership, while reducing unfair tax assessment of Black-owned property and providing adequate funding for public schools in rural communities.

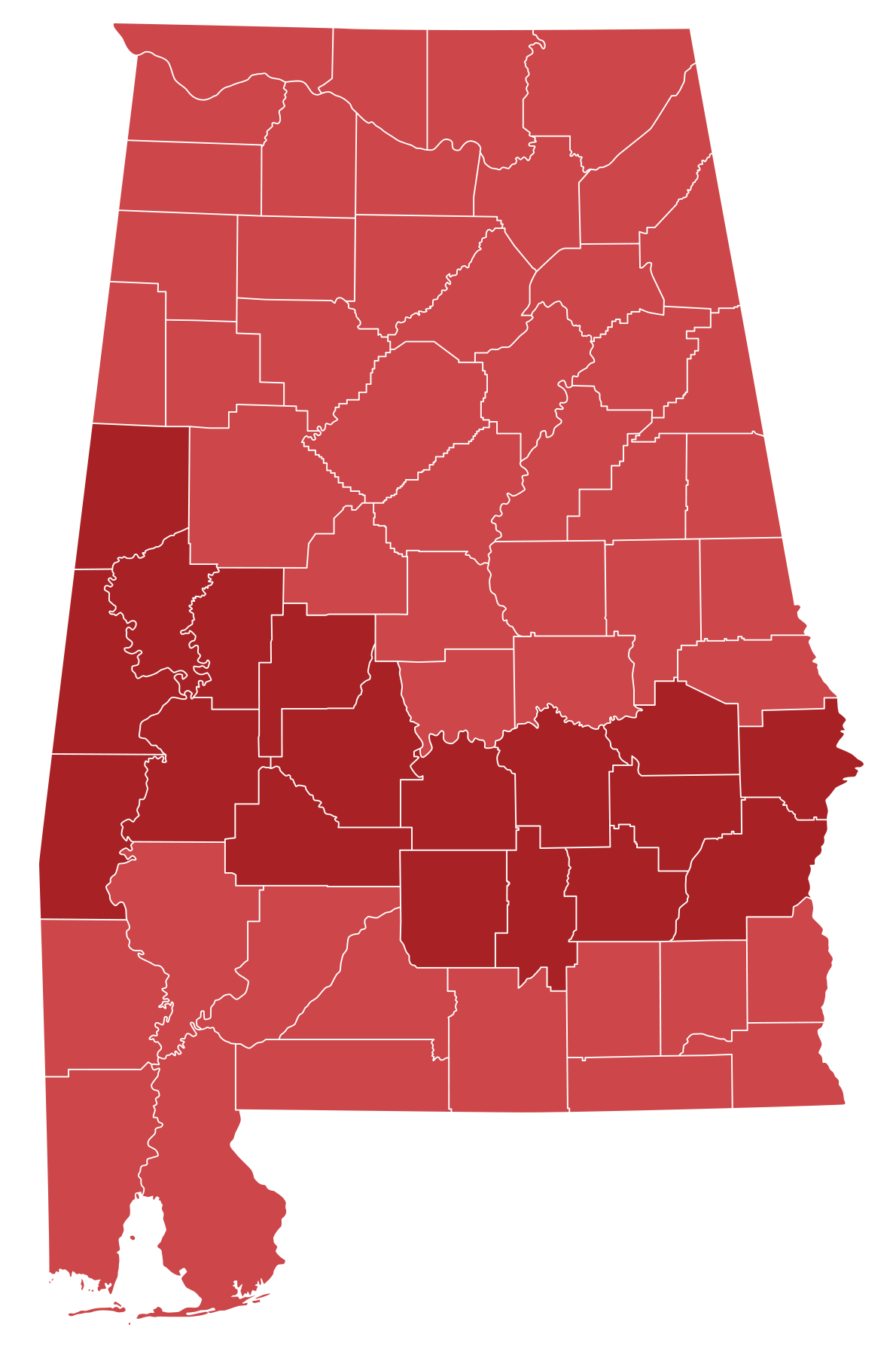

Alabama’s Black Belt region includes these 18 counties:

- Barbour

- Bullock

- Butler

- Choctaw

- Crenshaw

- Dallas

- Greene

- Hale

- Lowndes

- Macon

- Marengo

- Montgomery

- Perry

- Pickens

- Pike

- Russell

- Sumter

- Wilcox

How do Alabama’s property taxes measure up?

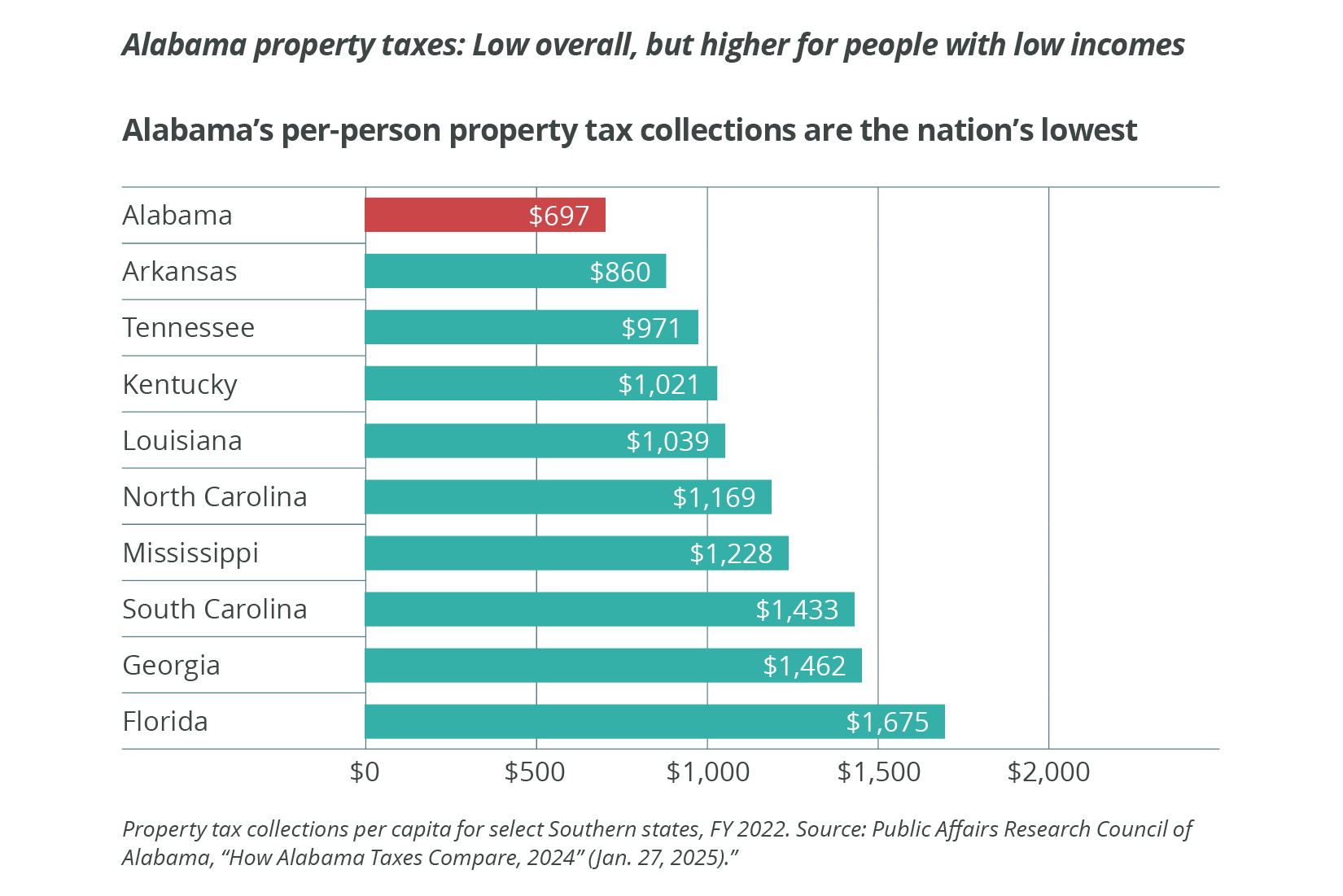

Alabama property owners overall pay the lowest combined local and state property taxes in the United States. In fact, the average combined taxes could double and still be below the national average. There are two main reasons for this ranking:

First, Alabama’s agricultural property tax breaks are poorly targeted. In the 1970s, rapid expansion of commercial and residential development increased the value of rural land near cities and towns. To keep property taxes on farms from skyrocketing, the Legislature created a set of formulas to assign discounted values based on current use of land. Alabama’s current use formulas allow landowners to pay far less than they would in other states. The maximum value per farm acre (for the best land) is $532 – unchanged since 1982. The maximum value per timber acre is $827.

Alabama’s agricultural landscape has changed in the last 40 years. Today, owners of giant corporate farms and timber holdings take advantage of discounts originally designed to protect smaller farmers. These discounts lead to severely undertaxed timberland, which contributes to the underfunding of health care, education and other valuable investments. Alabama places no limit on the size of a farm that benefits from reduced property tax rates. Georgia, by contrast, has a 2,000-acre limit on farms that qualify for a current use exemption. This cap protects family farmers while still ensuring equitable taxes on large corporate landholders. Alabama counties tax timberland at rates one-half of those paid by owners in similar counties in Florida, and only one-third of those paid by owners in similar counties in Georgia, Tennessee and Mississippi, according to a 2020 study by researchers at Auburn University and other institutions.

The severe undertaxing of Alabama’s timberland primarily benefits wealthy landowners – often large, profitable corporations – with limited ties to the community where their property is located. Nearly 60% of Alabama timberland is owned by people living outside of the county where the land is located. Alabama’s share of foreign-owned agricultural land in 2023 was 8%, more than twice the national average, according to the U.S. Department of Agriculture.

Second, Alabama’s constitution makes it hard for localities to raise property taxes but easier for them to increase sales taxes. Wealthy landowners and industrialists built barriers into the state’s 1901 constitution to shelter property from adequate taxation. Those barriers still exist, and the Lid Bill of 1978 made them even tougher.

How could we improve our state property tax?

Keep in mind: Alabama’s per-person property tax collections are the lowest in the nation. To fill the resulting funding gap, many communities have high sales taxes, which make our tax system more regressive. We need a better approach.

The property tax reforms below would help restore balance to Alabama’s upside-down tax system. Large landholders would pay more, while small-scale farmers would pay less. And Alabamians’ overall property taxes still would remain below the national average.

- Evaluate and update the state property tax rate. Property taxes are primarily a local revenue source but are subject to complex web of state restrictions. Many of these limits were erected by the 1978 Lid Bill and forgo revenue by providing large tax breaks to huge corporate landowners and wealthy homeowners. By contrast, the best form of relief are circuit breakers, which limit property tax liability to a certain share of income for households and renters with low and moderate incomes. In addition, many wasteful and ineffective property tax abatements for businesses need to be repealed.

- Increase overall property tax rates. Modest increases could generate a large amount of new revenue to strengthen public schools in communities across Alabama. One pathway would be to tax business property at the same assessment ratio as utility property. The state also could raise the minimum local millage rate for public schools from 10 mills to 20 mills.

- Protect homeowners with low incomes by increasing the homestead exemption. Excluding the first $50,000 of a home’s value from state taxes would provide a 25% increase in this exemption.

- Protect small-scale farmers by creating a “farmstead exemption.” This could be done by increasing the homestead exemption for a farmer’s home, or by creating a farmstead exemption that would protect average-sized family farms. Another option would be to create a new farmstead exemption for a certain number of specified improvements (such as irrigation systems).

- Adjust property taxes on timberland to bring them in line with surrounding states. Out-of-state investors own a substantial share of Alabama timberland, and they pay roughly a third of the property tax that their counterparts in Georgia and Mississippi do. Current use formulas set the value of Alabama timberland between $360 to $827 per acre depending on productive capacity. Alabama assesses timberland at 10% of these values for tax purposes, while the comparable figure is 40% in Georgia. Increasing the assessment rate to 20% for timberland holdings above 500 acres would protect most family timberland owners while raising revenue for counties to meet local needs.