How does state spending work?

One state, two separate budgets

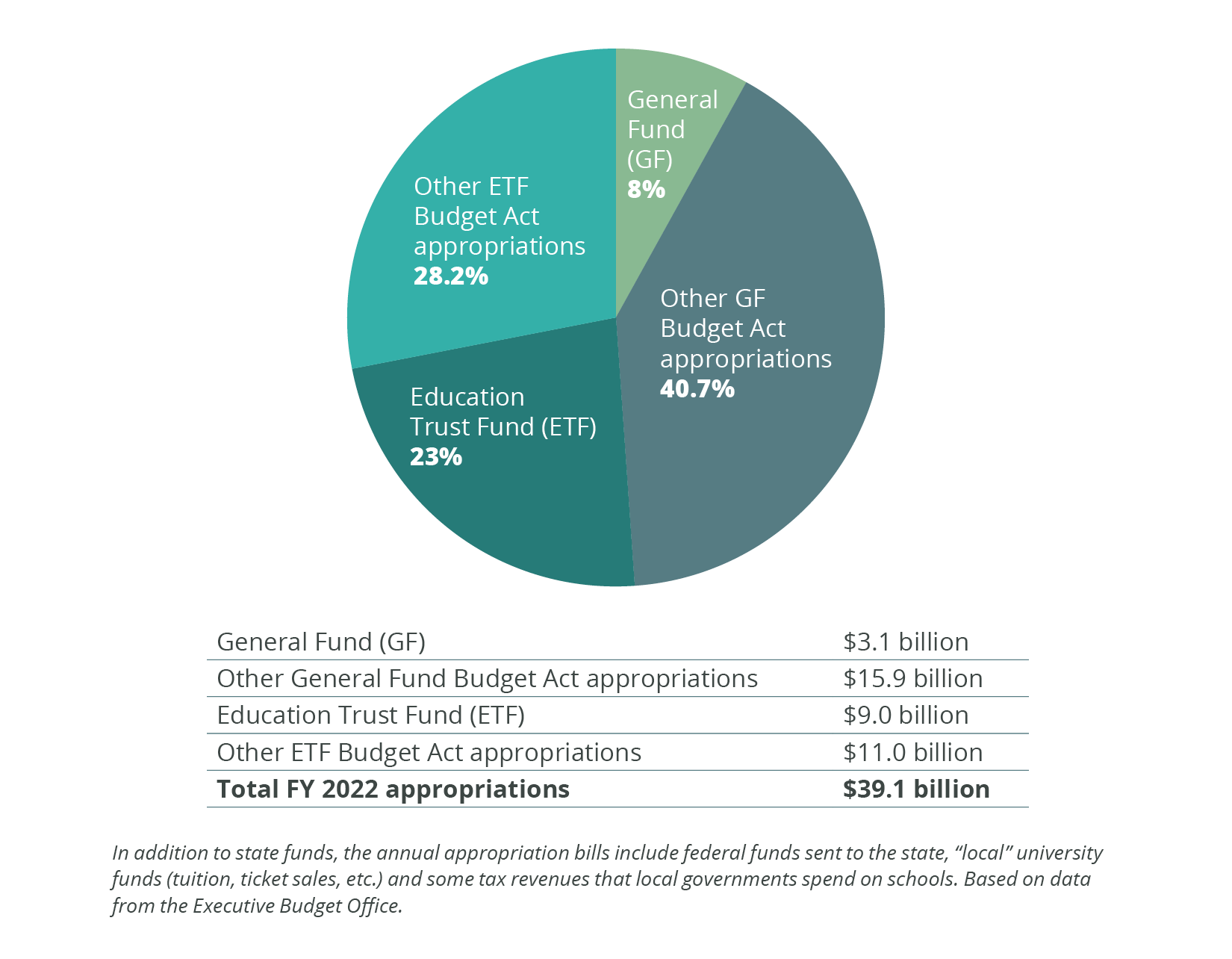

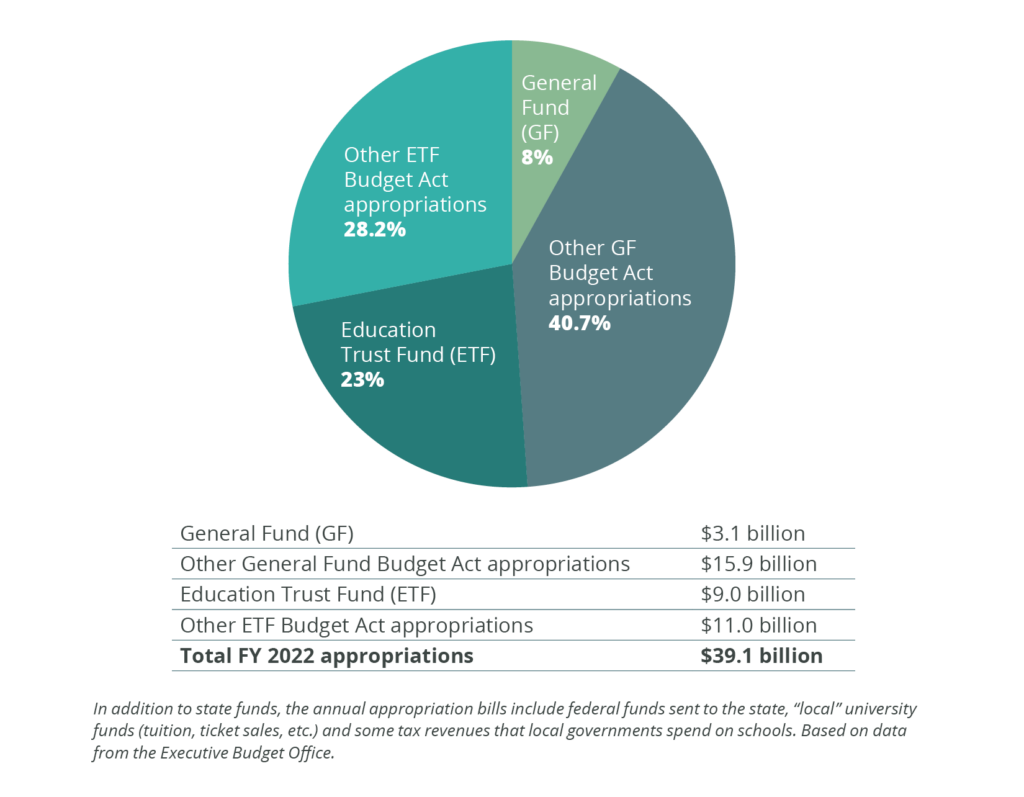

Of the Legislature’s $39.1 billion in total appropriations for fiscal year (FY) 2022, about $20 billion came under the Education Trust Fund (ETF) Budget Act for education-related services. Another $19 billion came under the General Fund (GF) Budget Act for all other services. Lawmakers also separately appropriated about $40 million in tobacco settlement money under the Children First Trust Fund to GF and ETF agencies (not shown on the chart). About 69% of total appropriations were earmarked, or set aside for a specific purpose, before lawmakers allocated them. Another 23% were designated for the ETF, though not earmarked for a particular purpose within it. Altogether, 92% of state revenue – everything outside the $3.1 billion General Fund – was restricted to some extent in how it could be spent.

It takes significant state and federal money to keep Alabama’s vital services running. Most of this money flows through the State Treasury. State agencies use the Treasury like a bank account. State and federal dollars appropriated by the Legislature are deposited there, and each agency draws out the money it’s been authorized to spend. Every penny the state spends goes through a formal budget process that involves the Legislature, the governor and state agencies.

Each year, the Legislature authorizes almost all state funding by passing two major pieces of legislation: the Education Trust Fund (ETF) Budget Act, which funds education-related services, and the General Fund (GF) Budget Act, which funds everything else the state does. (Lawmakers also pass several smaller budget bills annually.) Both major budgets include state tax revenues, as well as other state revenues like fines and fees and federal dollars. Each budget is divided into two parts: the smaller part controlled by the Legislature (discretionary funds) and the more significant part set aside by law for particular uses (earmarked funds). All federal funds are considered earmarked because the federal government, not the Legislature, decides where they can be spent. Because the Legislature must spend every dollar in the ETF on education-related programs, only the discretionary part of the General Fund budget is not earmarked.

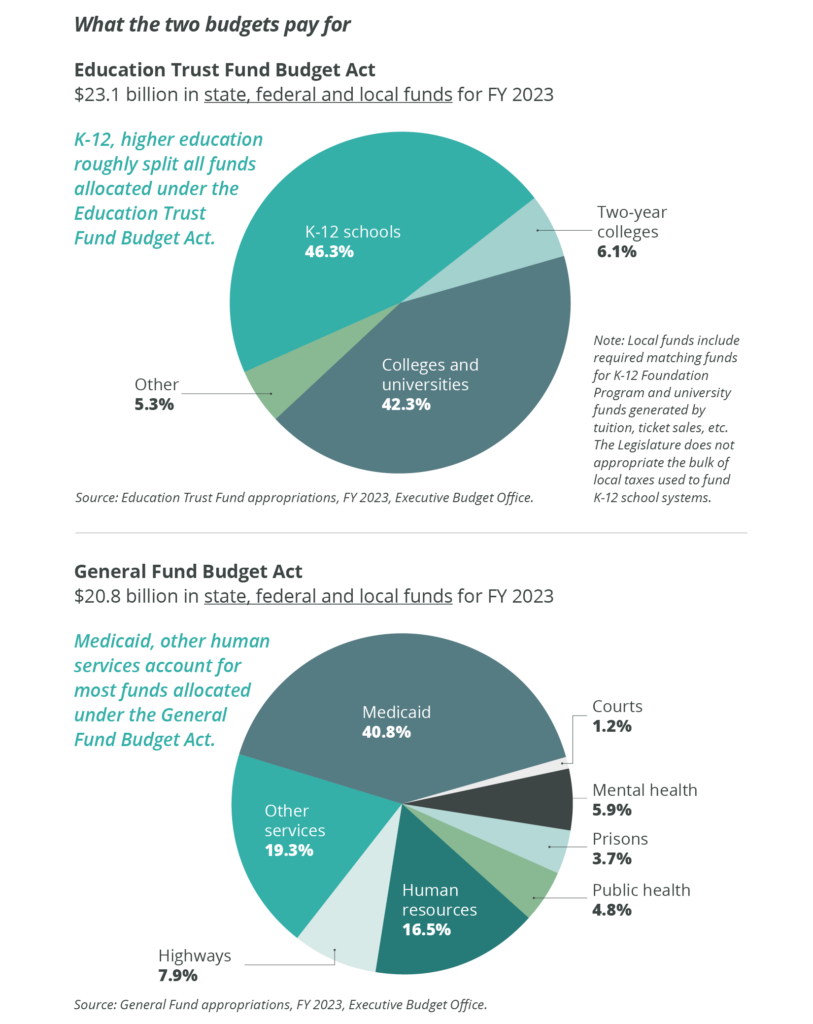

The annual Education Trust Fund Budget Act:

- Provides financing for all state education spending.

- Can be used only for education. Most funds are earmarked for particular education expenses, but lawmakers have some discretion over the areas of education on which the rest is spent.

- Often is referred to as simply the Education Trust Fund (ETF).

The annual General Fund Budget Act:

- Provides financing for all non-education programs.

- Primarily appropriates earmarked federal and state funds, including state gasoline tax revenues, which have been set aside for roads, bridges and traffic enforcement since 1952 under Amendment 93 of the state constitution.

- Includes the only state revenues that are not earmarked at all.

- Often is referred to as simply the General Fund (GF).

What state dollars pay for: Things that benefit all of us

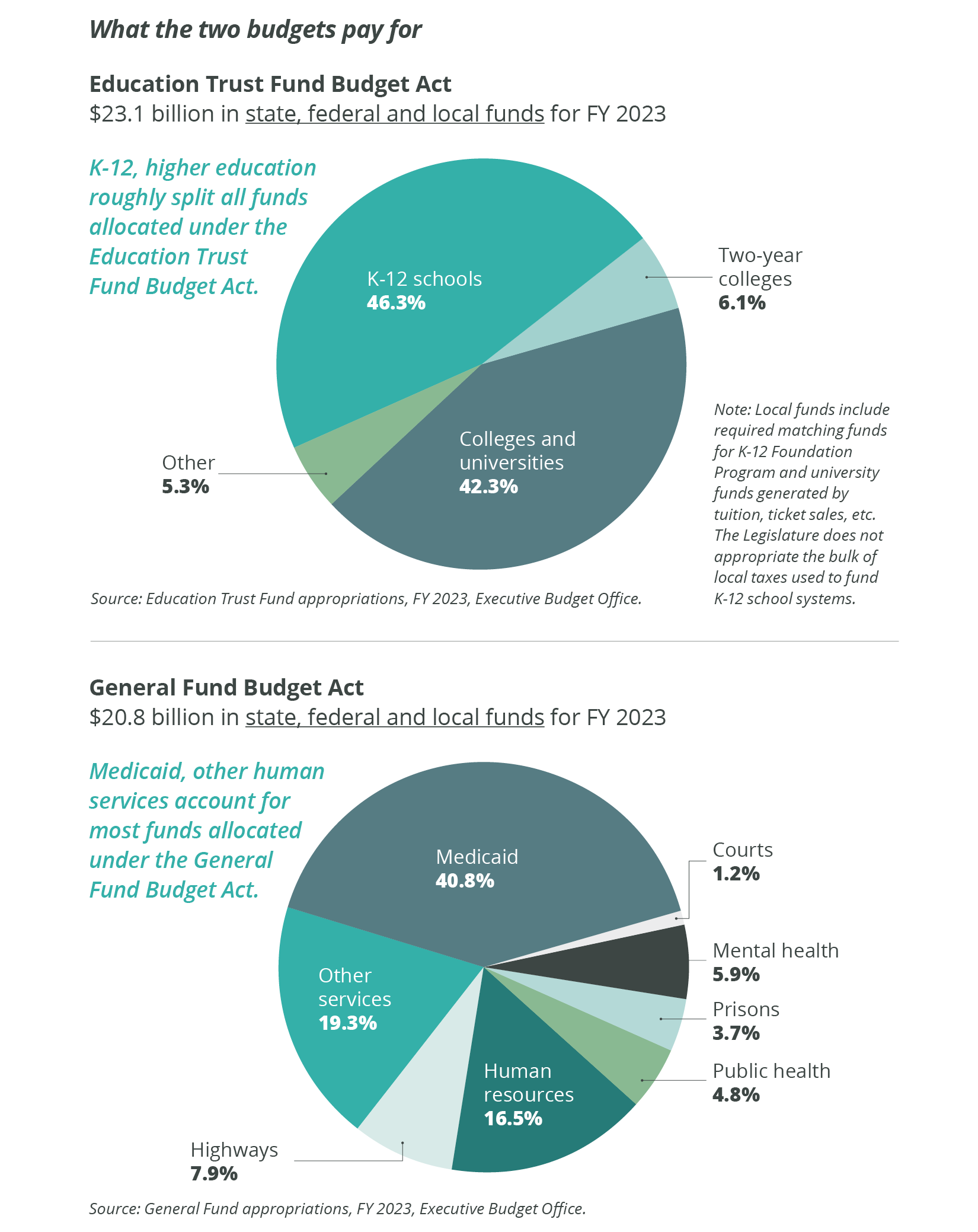

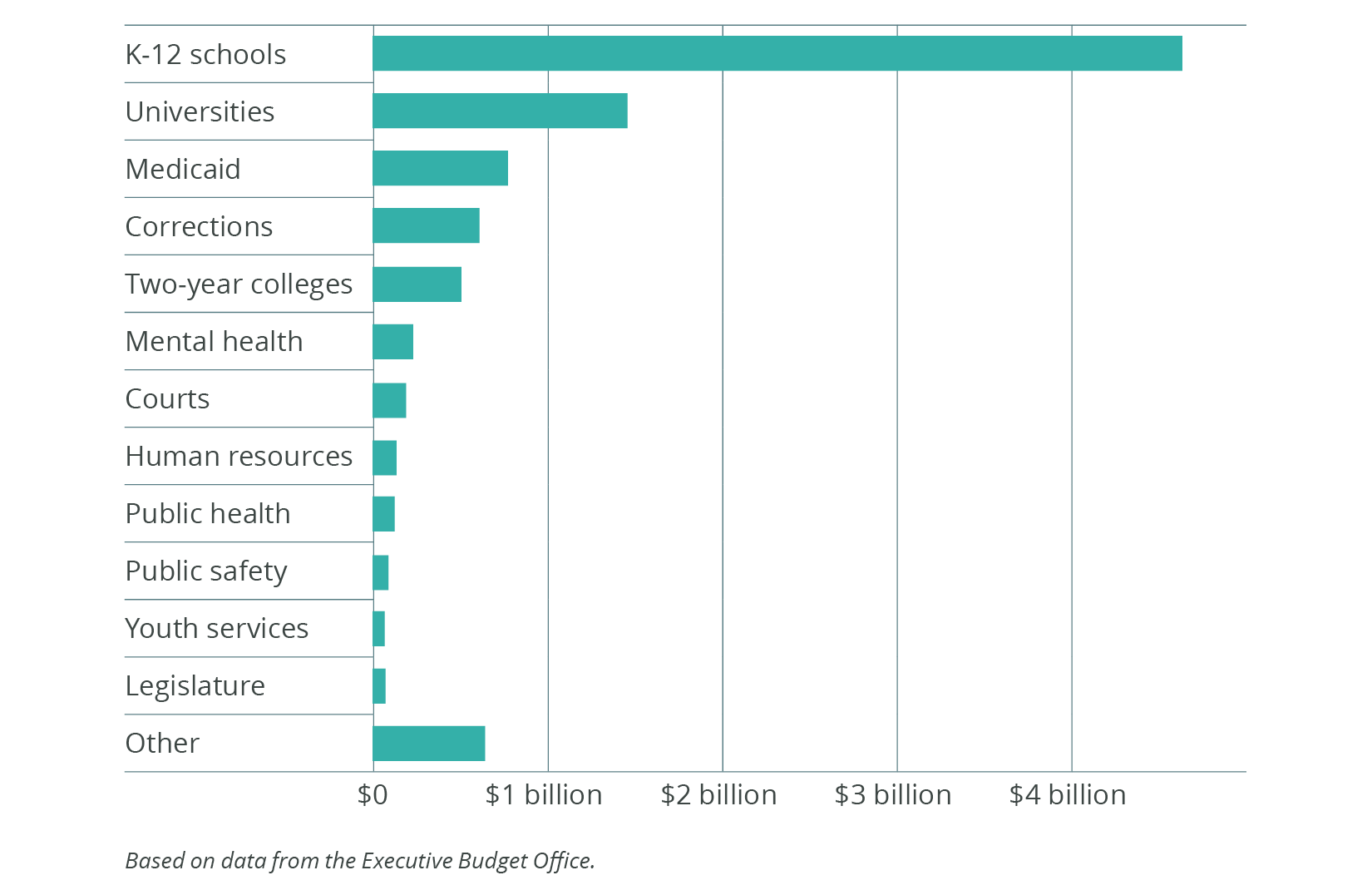

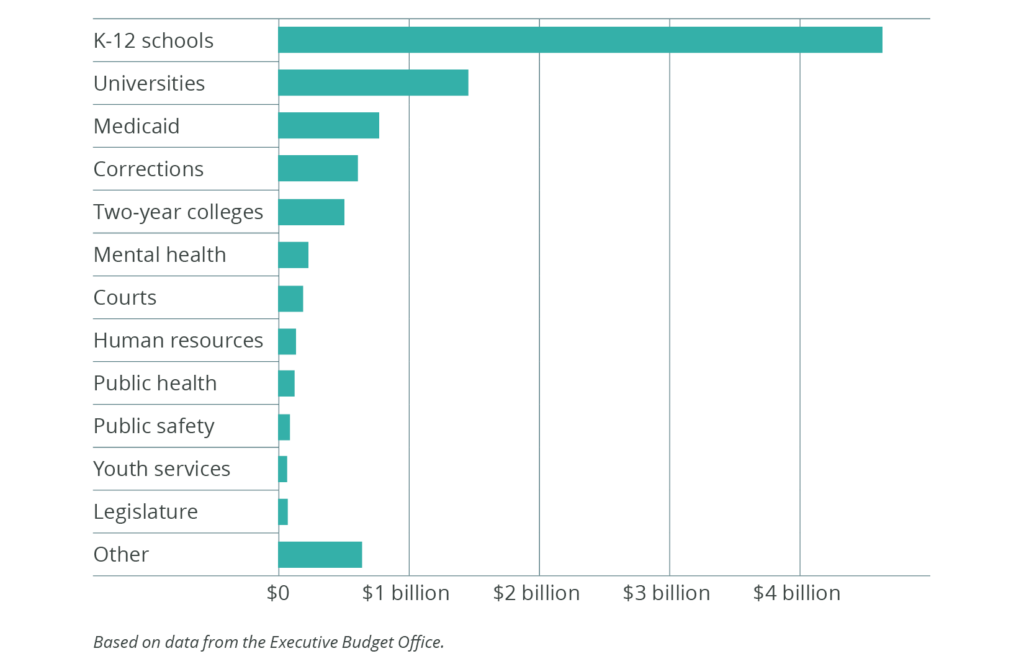

Education, health care, public safety and other vital services support economic growth and make our state a better place to live and work. Alabama spent $6.5 billion from the Education Trust Fund on K-12, colleges, universities and other education-related services in FY 2022. The same year, Alabama provided $2.2 billion in funding for Medicaid, mental health, courts and other non-education services from the General Fund. Of the total $8.8 billion, more than 75% of the funding went to K-12 schools and universities, easily exceeding the amount that went to Medicaid, corrections and other General Fund services. Here’s a look at what state dollars supported:

In FY 2022, Alabama spent $6.5 billion from the Education Trust Fund, mostly on K-12 and higher education. This easily exceeded the amount that went to Medicaid, corrections and other vital services from the General Fund.

In passing the General Fund Budget Act each year, the Legislature is most concerned with the discretionary funds (dollars that are not earmarked) that make up what legislators call the General Fund (GF). Even though this money amounts to only a small portion of total GF Budget Act spending, it’s the portion that lawmakers are free to debate and divide up to help meet the state’s many competing needs. The Legislature seeks input from agency leaders and the general public in assessing these needs.

In most states, the Legislature has relatively wide latitude in deciding how to spend the money from state taxes. But Alabama lawmakers’ choices are much more limited. Over the years, Alabama voters have placed severe restrictions on how tax dollars are used by designating them (in constitutional amendments and statutes) for specific purposes. While this earmarking can help safeguard against misuse of state funds, it also can prevent legislators from creating a budget that adequately meets current needs for education, public health and other services that improve lives and build Alabama’s economy.

Tax expenditures reduce funding for essential needs

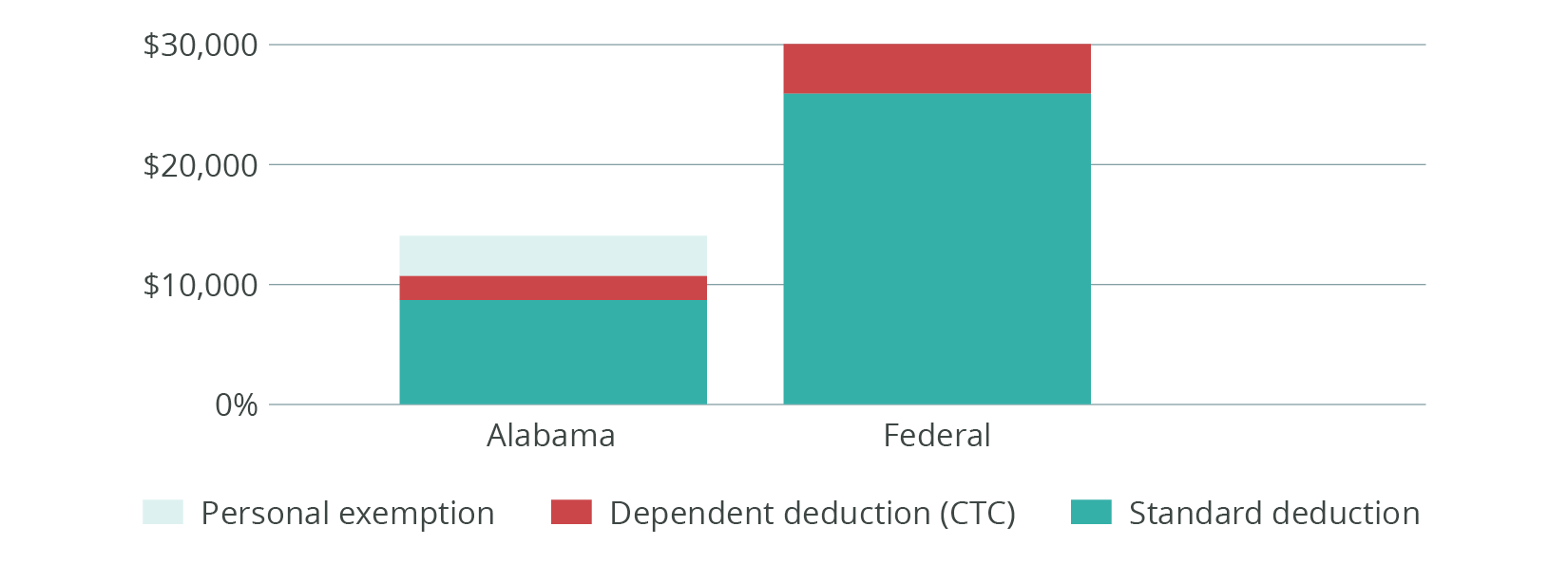

State tax incentives, tax credits and tax exemptions significantly affect state budgets by reducing the amount of money the Legislature can appropriate. These tax expenditures benefit specific companies, businesses or individuals and can total hundreds of millions of dollars annually. The Legislature routinely passes dozens of bills each year that exempt items such as farm supplies from sales taxes, direct tax credits to new and existing businesses, and create broad tax credits that reduce essential revenue.

One example of a tax credit with a significant budget impact is the CHOOSE Act, enacted in 2024. The law provides eligible parents with up to $7,000 per child each year for private schools and up to $2,000 per child each year for homeschooling. Those credits are available even for parents whose children never attended a public school. The CHOOSE Act will divert between $150 million and $200 million a year from public schools through 2027-28. That amount is enough to pay for up to 2,500 teachers every year. And the cost could grow in future years if lawmakers increase or remove the income cap for eligibility.

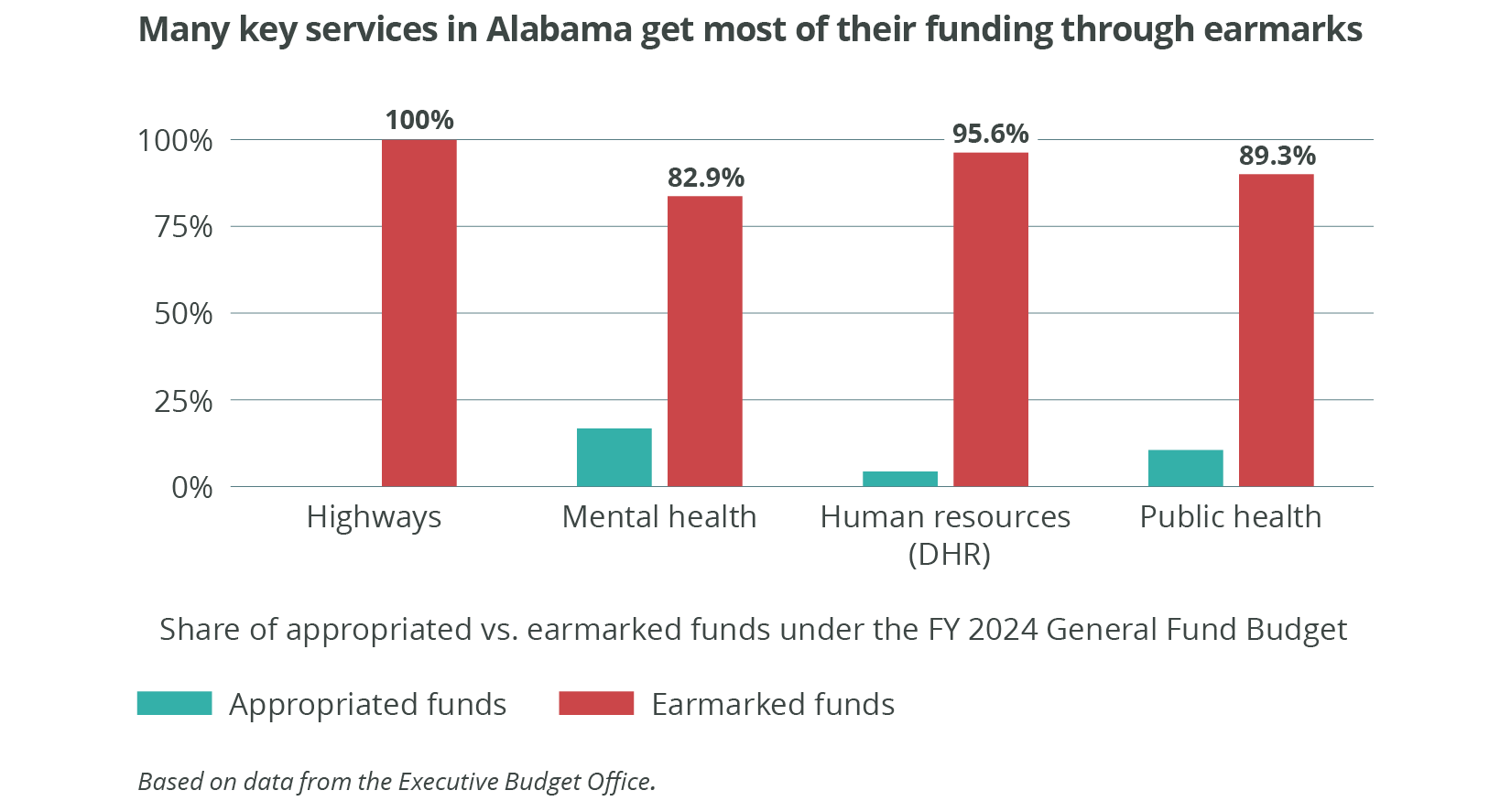

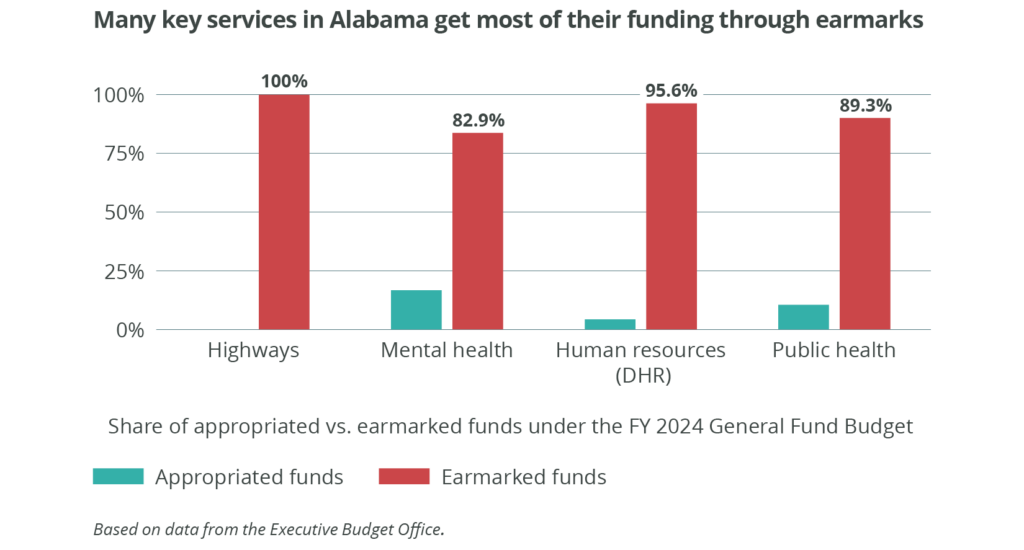

Earmarked vs. appropriated funds

Some major agencies in Alabama depend significantly more on earmarked funds than on appropriations from the Legislature. This ensures stable funding for services, but it reduces the Legislature’s ability to create a budget meeting current needs.

When revenues fall below the amount needed to maintain services, the state must choose from a short list of options: Find one-time revenue sources, tap reserve funds, cut services or raise taxes. The state constitution prohibits Alabama from using money in any earmarked account to pay for other services. (Imagine not being able to use the money you budgeted for a birthday party to have a leaky roof repaired!) Alabama does have several “rainy day” reserve funds that have helped prevent proration, or mid-year service cuts, during the last decade. The most significant of these came in the Rolling Reserve Act, which was passed in 2011 and revised several times since. The law caps annual education spending and moves any remaining funds into reserve accounts and an account that can be used for non-recurring expenditures.

Most other states have much more flexibility in allocating spending for different programs. Reducing earmarking would make Alabama’s budgets more responsive to changing needs and priorities. But most earmarking changes would require amending the constitution or writing a new one. Constitutional amendments require voter approval, which may be difficult to get because many voters support earmarking as a check on legislative power.

Racial inequity at a glance

Alabama’s seven constitutions have recognized the importance of public education and, until 1955, encouraged education. Following the U.S. Supreme Court’s landmark Brown v. Board of Education decision, however, Alabama revised its constitution to say that “nothing in this Constitution shall be construed as creating or recognizing any right to education or training at public expense.” This was a direct act of defiance intended to maintain a racial hierarchy and the vestiges of white supremacy in Alabama. Though courts ruled school segregation unconstitutional, subsequent cases have failed to establish a clear right to equitable education funding throughout the state. Education funding in Alabama still varies widely based on the wealth, and racial makeup, of local communities – especially when it comes to revenues from local property taxes.

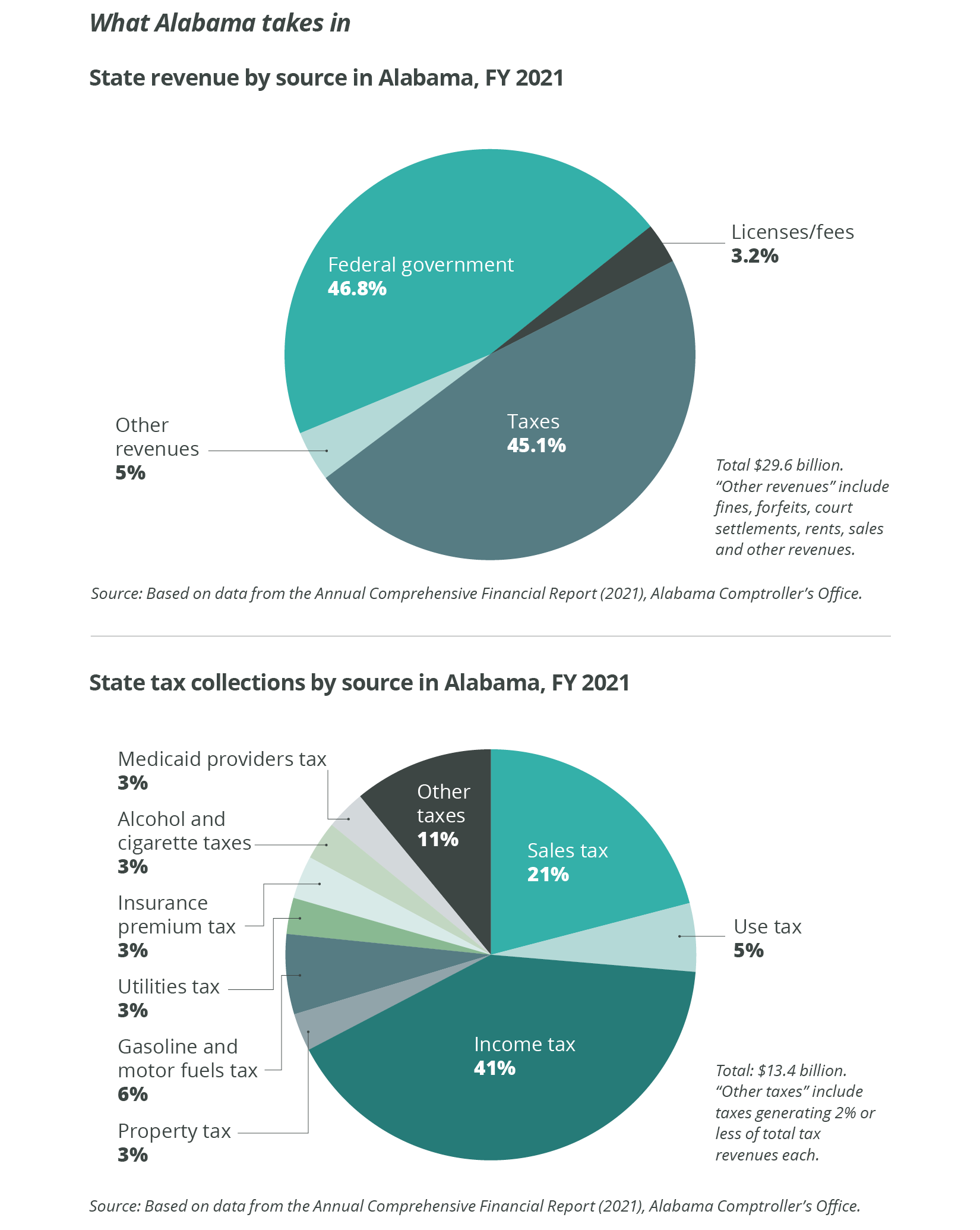

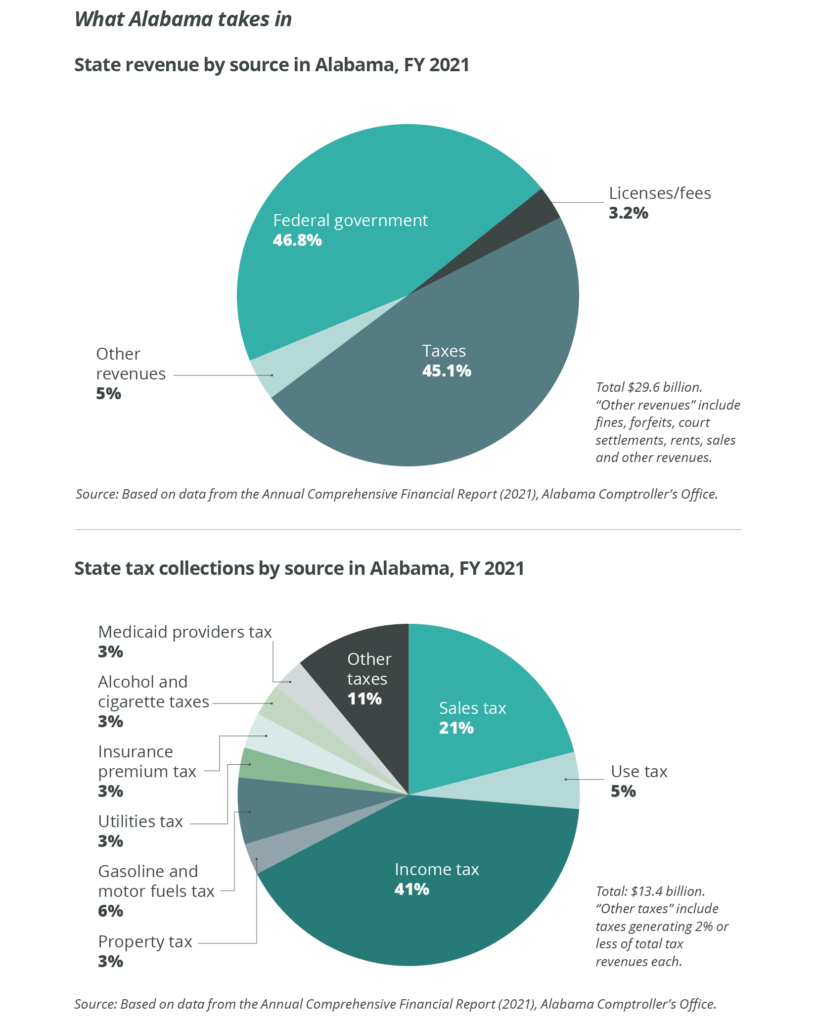

Where does the state get its money?

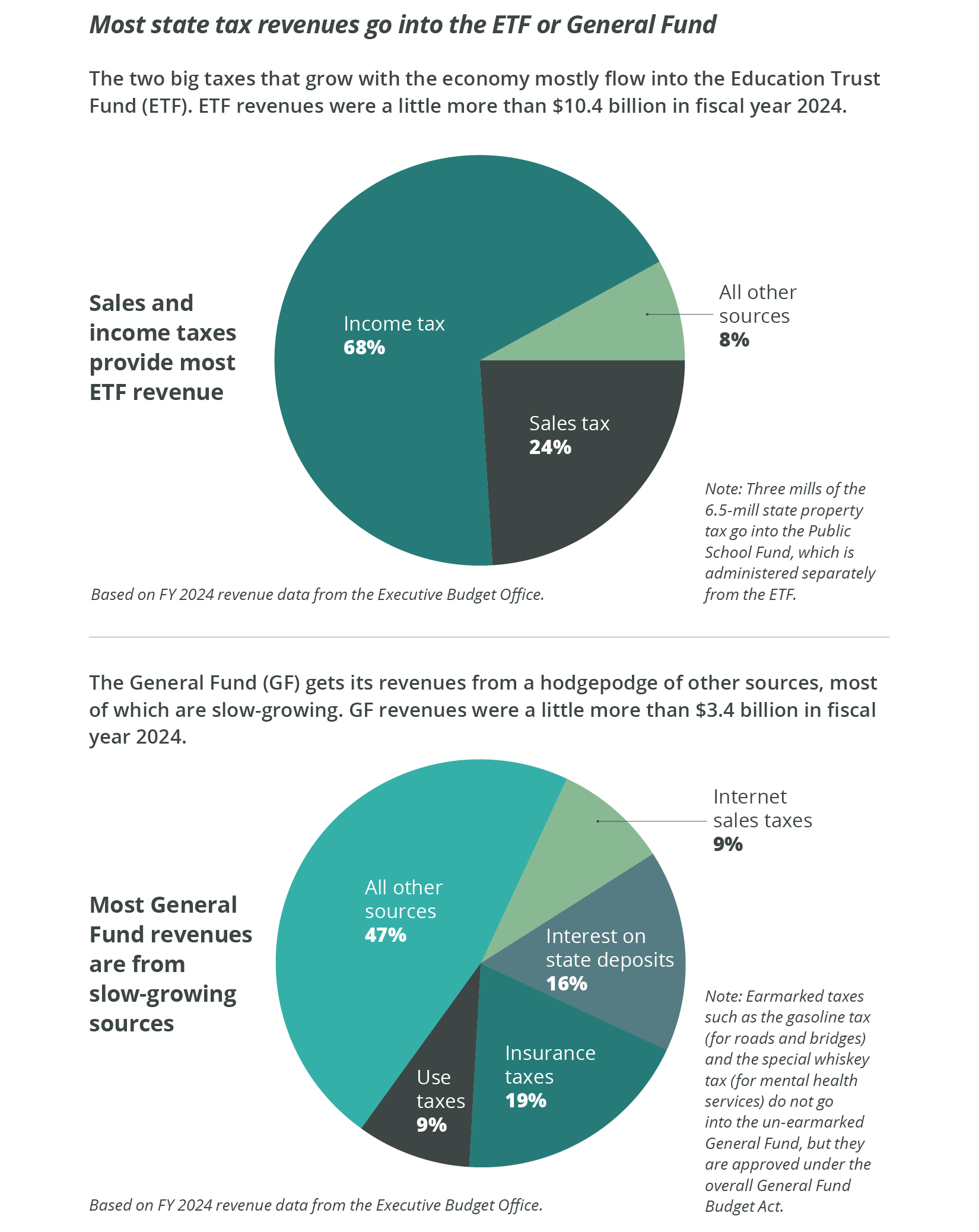

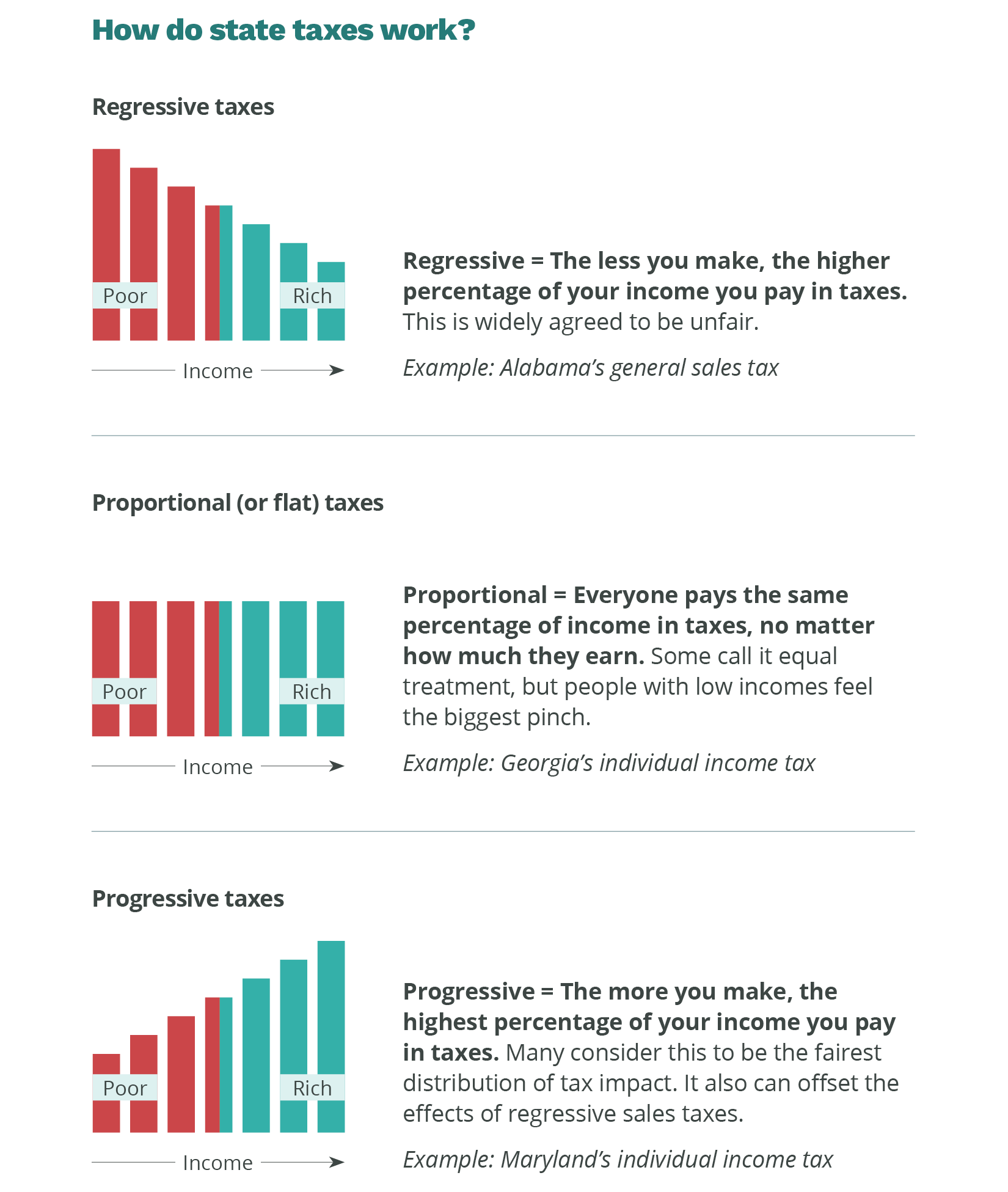

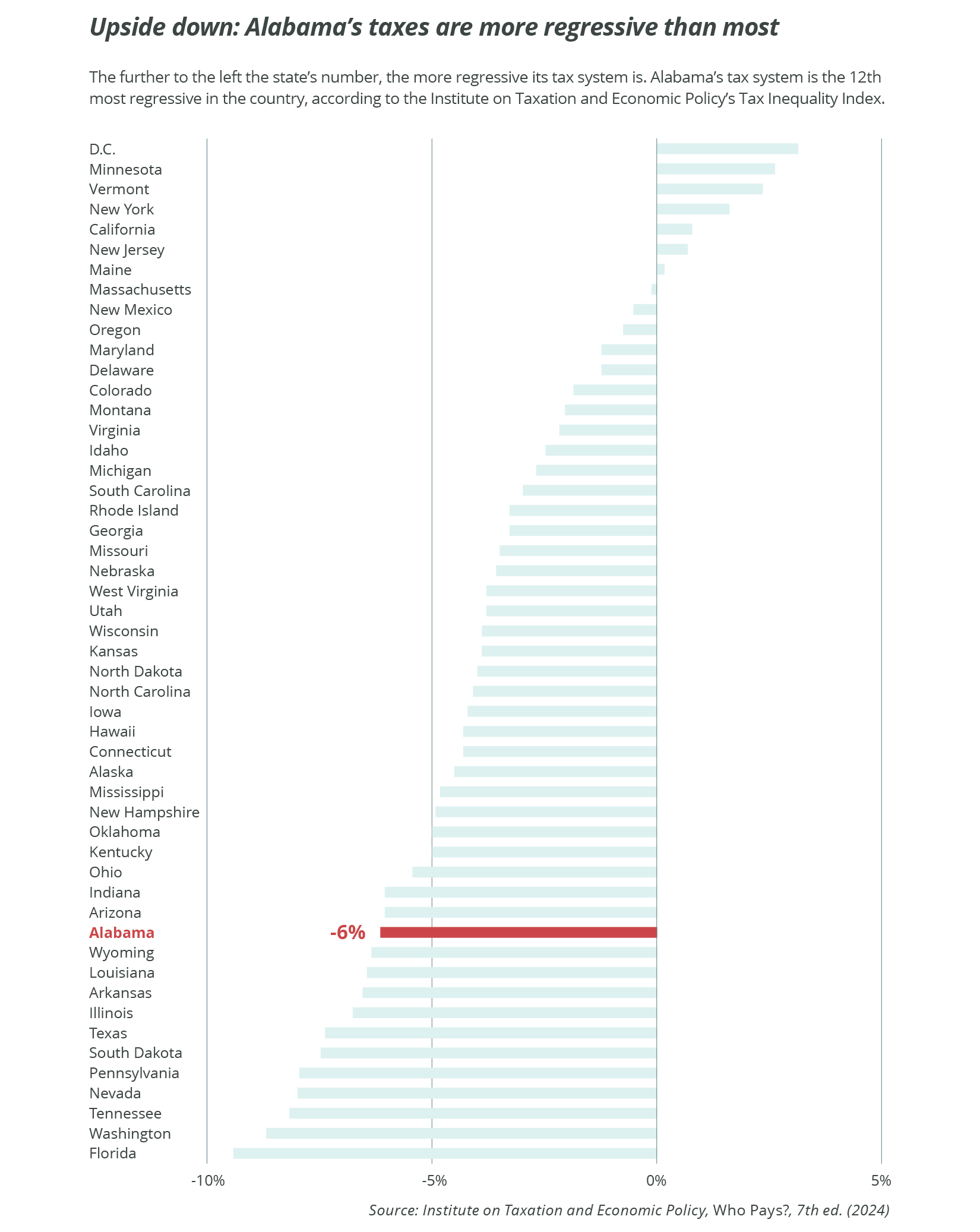

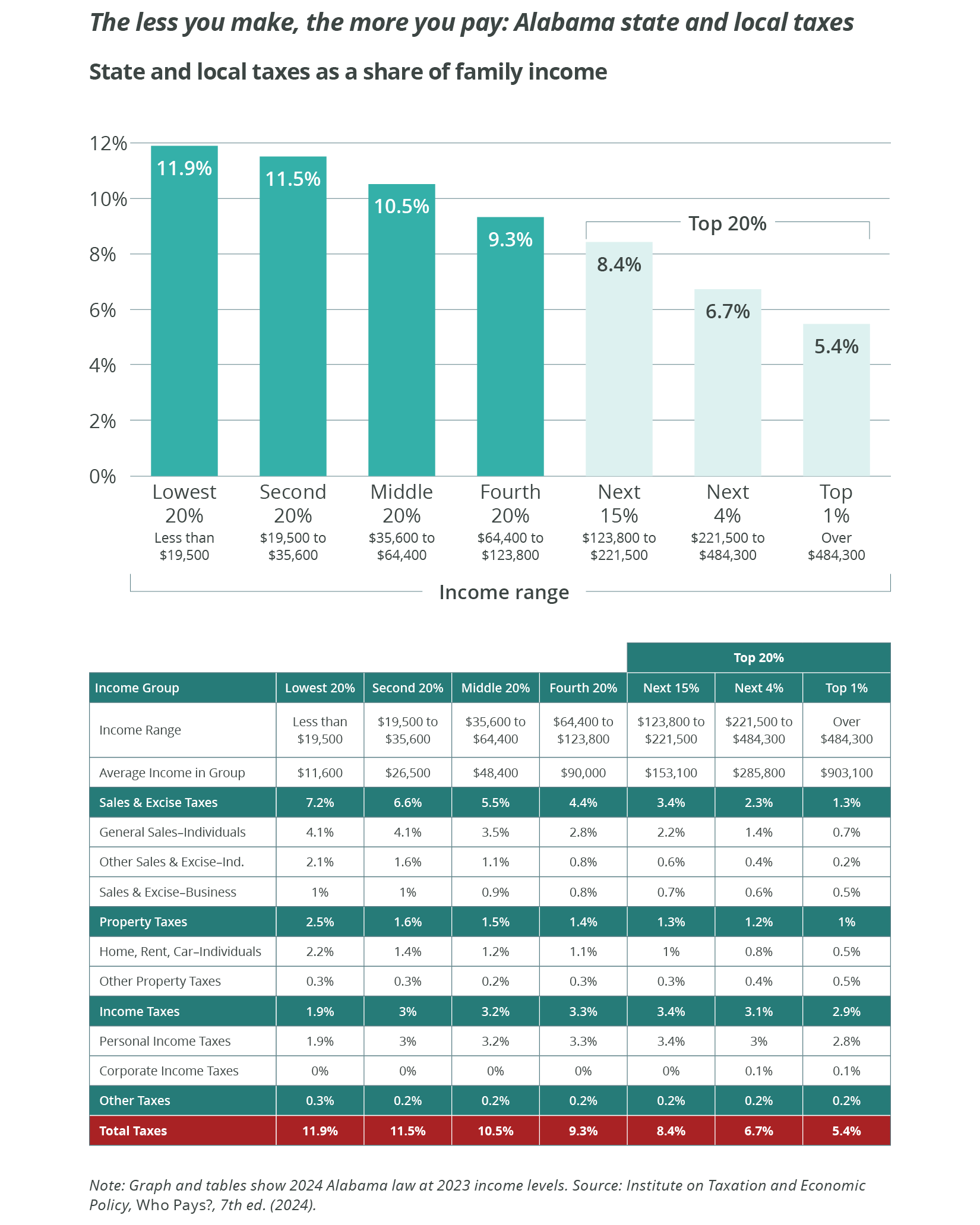

- From us – More than half of all the money Alabama takes in every year comes from taxes and fees that individuals and businesses pay. The lower graph on in the image above shows the share of this revenue that each state tax garners. (Note: The graph does not include local tax revenues, which in recent years have equaled a little less than half of the amount collected by the state. In Alabama, as in most other states, the property tax is mainly a local tax.) For a look at how state taxes work, see the image below.

- From the federal government – More than 45% of Alabama’s budget dollars ($2.25 of every $5 the state spends) comes from Washington, D.C. This is higher than in most other states. On average, states receive 35% of their budgets from the federal government. (Worth noting: During the COVID-19 pandemic, states witnessed an increase in federal financial support. Historically, only about one-fourth to one-third of states’ budgets have come from the federal government.) These are dollars that the federal government provides to help the state support basic services like education, health care and transportation. Most federal grants require a state contribution: When Alabama spends a certain amount on a particular area, the federal government will provide “matching” funds. The more the state spends, the bigger the federal match (up to a point).

Because Alabama’s state spending is so low, we often contribute little more than the minimum amount necessary to receive federal matching funds. In some areas, we forfeit the federal match altogether by failing to provide a state match. Most other states take better advantage of the match by contributing more state dollars to federally supported programs. A prime example: Alabama is one of only two states providing no state money for public transportation. That means our state forfeits tens of millions of federal dollars every year. It’s money that could support buses, trains, ride-sharing services and other efforts to help thousands of families stay connected. Even a modest state investment would help Alabama draw down tens of millions of federal dollars to help families get to work, the doctor’s office or wherever else they need to go.

Because Alabama’s state spending is so low, we often contribute little more than the minimum amount necessary to receive federal matching funds.

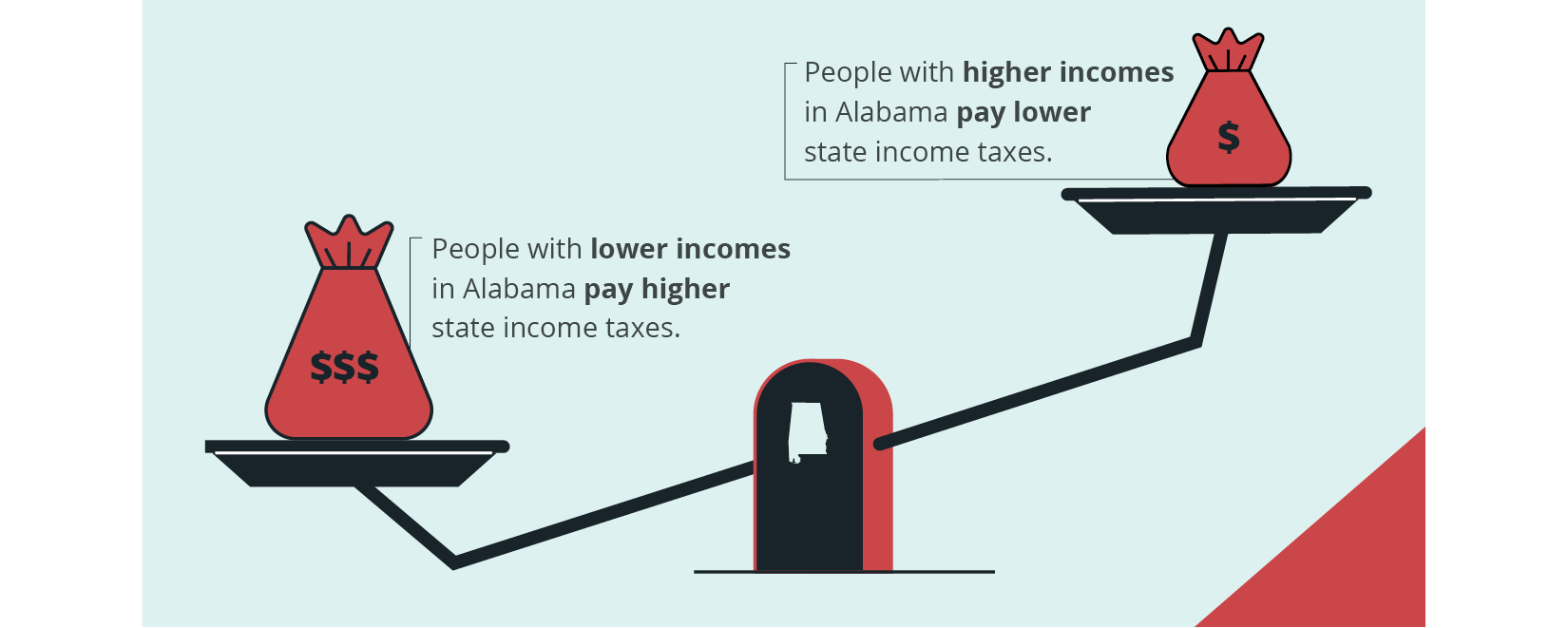

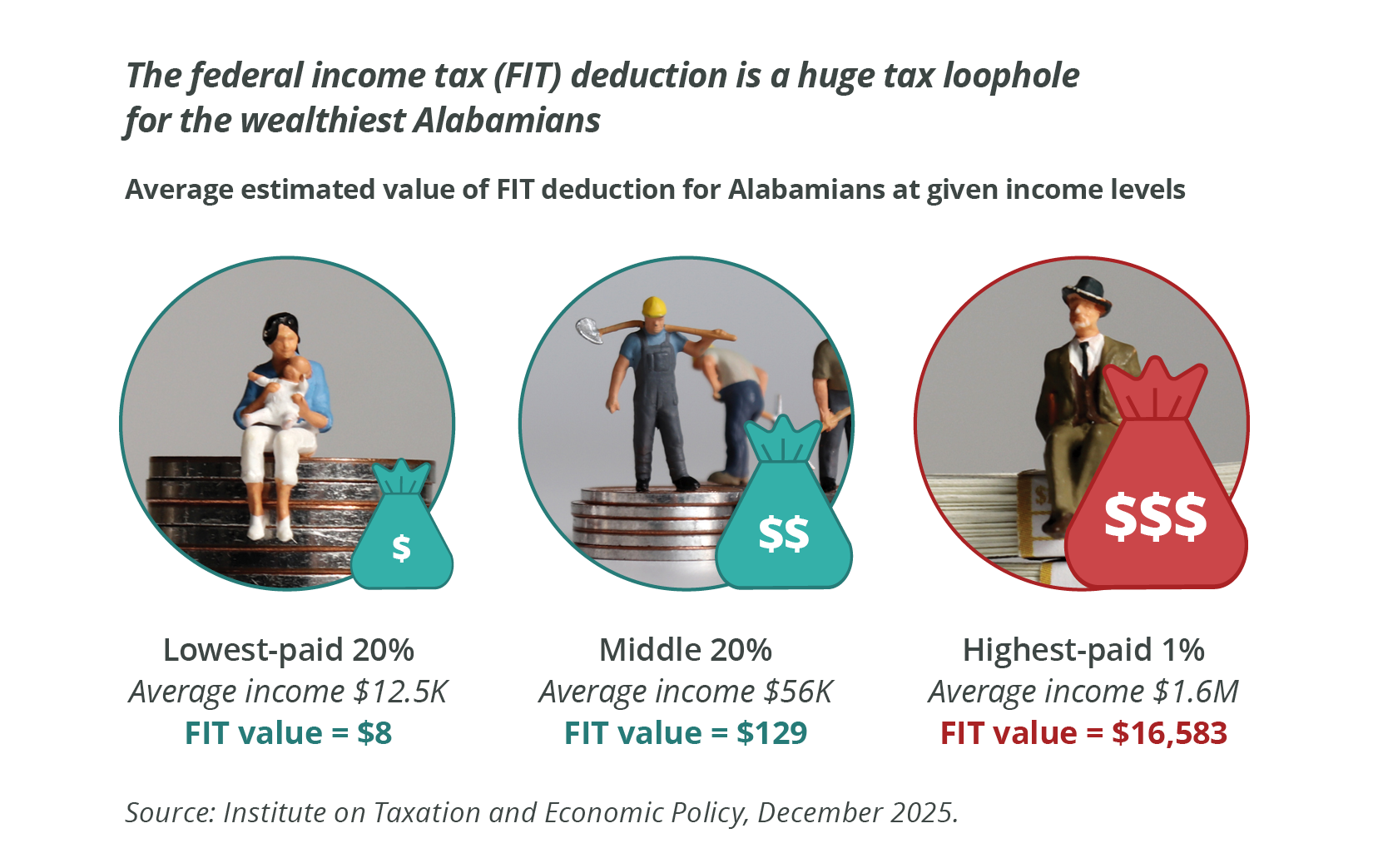

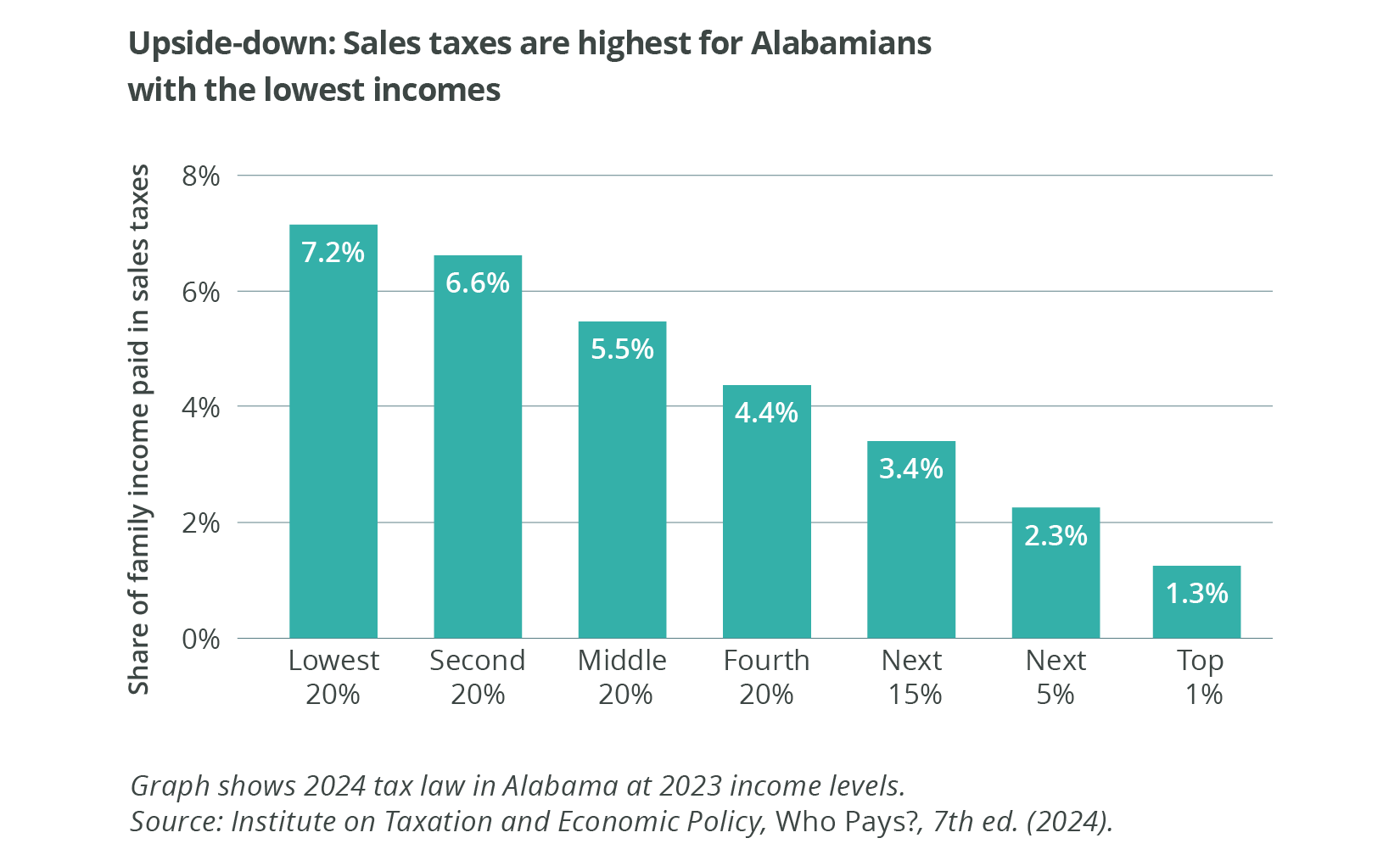

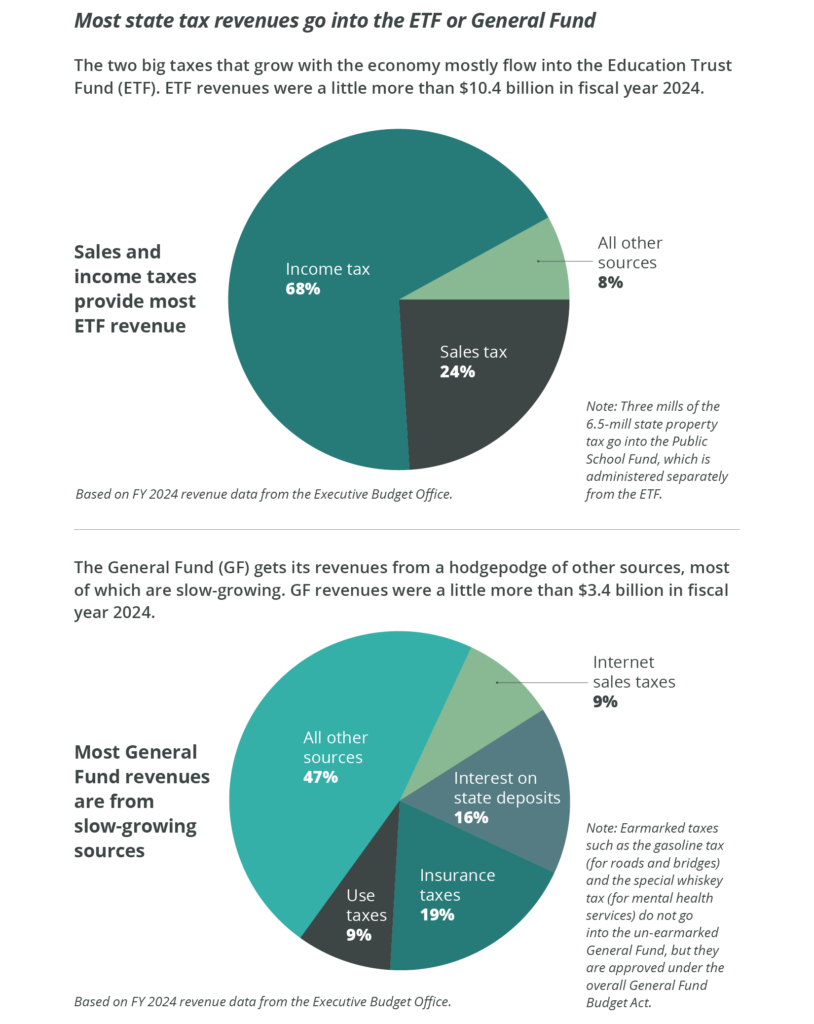

In Alabama, some state programs and services have more adequate funding than others, and some years have more adequate funding than others. Tax revenues that grow with the economy (major taxes on consumers and workers, such as sales taxes and income taxes) are largely earmarked for the ETF. This imbalance has improved in recent years because revenues from internet sales taxes (called the simplified sellers use tax) have increased, providing new “growth taxes” for the General Fund. In addition, post-pandemic revenue growth has allowed lawmakers to continue funding state services while enacting a one-time income tax rebate and a permanent reduction in the state sales tax on groceries. These revenue increases may not be sustainable in the long term, however, and income taxes and most state sales taxes remain earmarked for education.

Other state services under the GF continue to get the leftovers – an assortment of minor taxes, interest and fees, many on businesses, that often grow at a sluggish rate. The slow growth keeps services like Medicaid and corrections permanently shortchanged as costs continue to grow. There’s also a disadvantage to the ETF’s reliance on sales and income taxes: In bad years, they can shrink. Many states, including Alabama, set aside money in good years in a rainy day fund to help them in bad years.

Alabama has created rainy day funds by drawing from the Alabama Trust Fund – which gets revenue from offshore oil and gas drilling – and by using money that exceeds the ETF spending cap under the Rolling Reserve Act for school infrastructure and one-time expenses like buses and textbooks. Alabama also has established a Budget Stabilization Fund in the ETF where revenues in excess of the appropriation cap are transferred and a General Fund Budget Reserve Fund in which up to $100 million can be deposited to prevent proration. In 2023, the Legislature created a new education reserve fund called the Educational Opportunities Reserve Fund.

Despite these improvements, Alabama’s inadequate budgets for core services point to a deeper problem that can’t be fixed easily: The state doesn’t have enough money each year to support state services adequately or to expand services to meet a growing population or address new needs. This built-in shortfall is called a structural deficit. A more adequate tax system would bring in enough stable revenue to help prevent shortfalls and give legislators more leeway to respond when they occur.

The structural deficit shows how our state’s fiscal system has failed to keep up with changing times. In the budget crisis of 1933, the Legislature began dealing with revenue shortfalls by using proration, or cutting current spending (except for teacher and state employee salaries) across the board. By requiring the governor to use proration to avoid deficit spending, the law spares legislators from making tough decisions on which services should bear the brunt of cuts. For schools, though, the effect can be dramatic: Ordered in June to cut $10 million in spending for a budget year that ends Sept. 30, a system may be forced to choose between replacing worn-out roofs or replacing old math books. Alabama has used proration 18 times since 1975 but has not had to prorate the education budget since the Rolling Reserve Act was passed in 2011. However, the state had to borrow from the Alabama Trust Fund during recent difficult budget years and had to draw money from the ETF Budget Stabilization Fund during the pandemic recession.

Racial inequity at a glance

Alabama’s funding of our court system relies heavily on money collected from the users of the system. These fees include civil and criminal court costs charged against people – disproportionately Black – caught in the legal system. Some of these court costs are sent to the state General Fund (GF) and help fund local courts and related agencies. In 2022, Alabama’s state court cost collections were more than $60 million. While the exact appropriation of these fees is unclear, the $60 million collected equaled 28% of the GF appropriation to Alabama’s trial courts.

This heavy reliance on court costs to support the justice system negatively impacts the state. It encourages law enforcement and courts to focus on collecting revenue to support their operations. People of color and people with low incomes are disproportionately caught up in the justice system, in large part due to overpolicing in these communities (rather than either group committing crimes at rates higher than their counterparts). As a result, the weight of funding our courts falls heaviest on the people least able to pay. A 2018 study by Alabama Appleseed found that more than 80% of people surveyed gave up necessities like rent, food, medical bills and child support to meet their court debt.

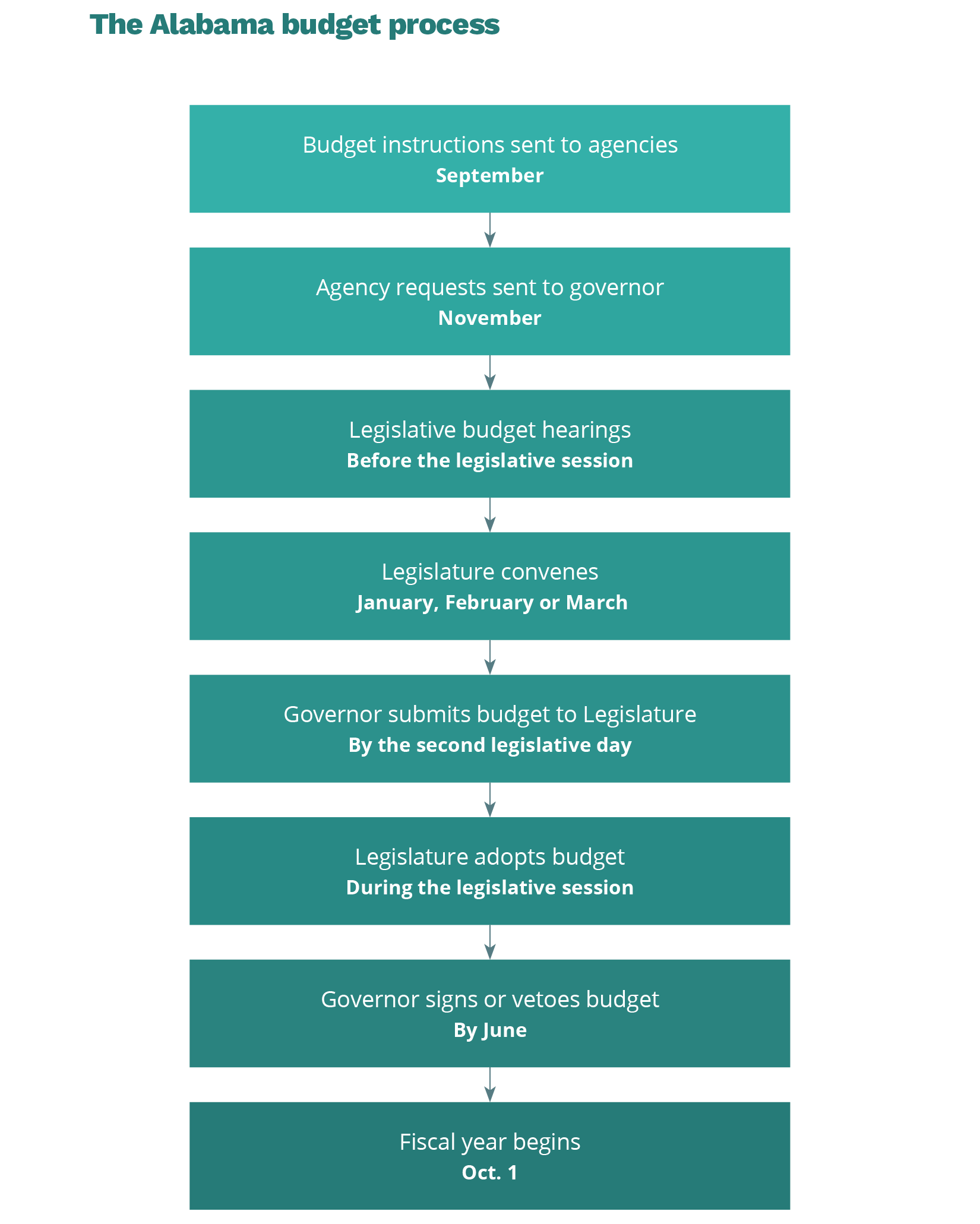

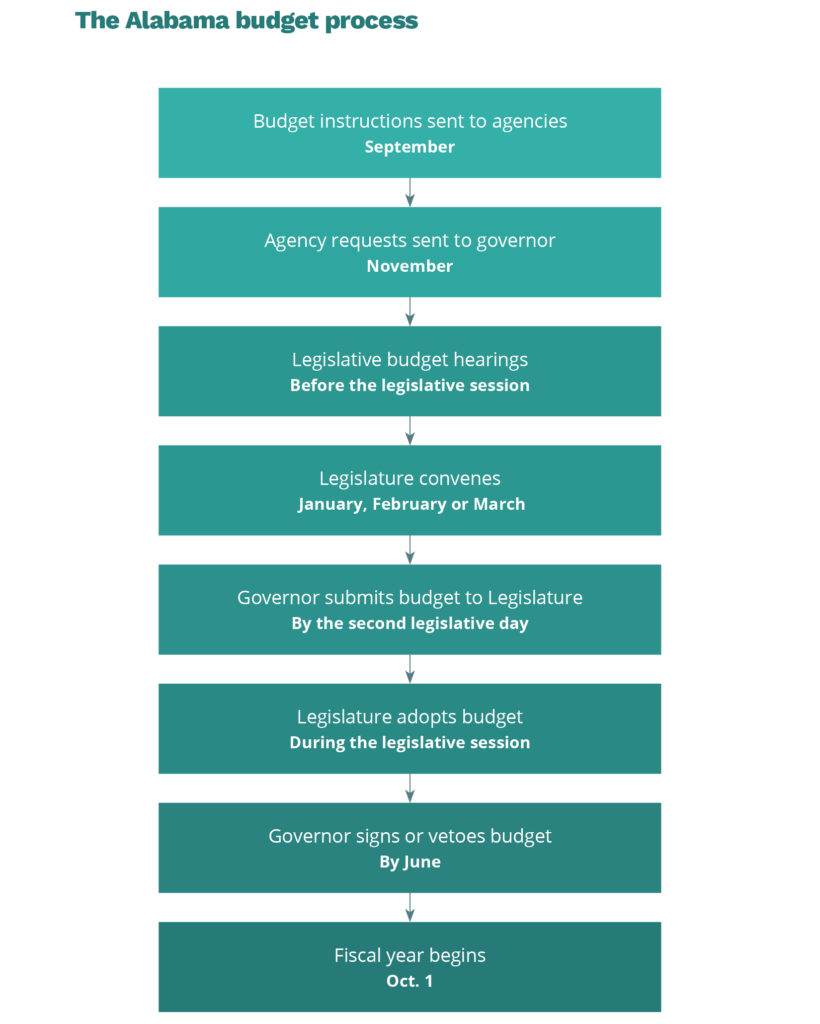

The Alabama state budget process

Each year, the governor prepares a financial plan and introduces two major budget bills: a General Fund (GF) bill and an Education Trust Fund (ETF) bill. In the plan, the governor outlines budget priorities, revenue projections and updates on the past fiscal year, which runs from Oct. 1 to Sept. 30. The governor drafts the plan after considering each state agency’s programmatic and financial objectives. The plan also includes recommended revenue measures to ensure a balanced budget. The governor must present a proposed budget to the Legislature on or before the second legislative day of each regular session of the Legislature.

After receiving the governor’s budget proposal, the Legislature:

- Considers the governor’s recommended plan.

- Adopts alternatives or revisions to the governor’s plan.

- Passes legislation to authorize budgets for the next fiscal year.

After the introduction of the governor’s plan, the Legislature has until the end of a regular session to pass the budgets. This period of approximately three months – a comparatively short timeframe for consideration and passage of the state’s multi-billion-dollar GF and education budgets – is the critical period for public comment on the state’s spending priorities. During a regular session, the Legislature meets (usually on Tuesdays and Thursdays) for a maximum of 30 meeting days during a period of 105 calendar days. If lawmakers fail to pass one or both of the budgets during the regular session, the governor may call the Legislature back for a special session.

Both the House and Senate have separate budget committees that review and vote on the ETF and GF budgets. These budget committees often make significant changes to the governor’s proposed budget. State agencies, the governor’s Department of Finance and the Legislative Services Agency (LSA)’s Fiscal Division appear before these subcommittees with reports and recommendations. These committee hearings are the one of the best times for Alabamians to voice their opinions. The committees most often meet on Wednesdays.

Alabamians can voice their opinions on the budgets by:

- Calling their legislators’ district or Montgomery office number.

- Writing a letter.

- Meeting with their legislators or a member of their staff.

- Sending an email.

- Requesting a public hearing on a budget expenditure.

- Testifying at a scheduled public hearing on a budget.

Each chamber discusses and votes on the budget bills separately. It is common practice for one major budget to “originate” in either the House or Senate and the other major budget to begin in the other chamber. The committees considering the budgets review the governor’s proposals and any changes approved by the other chamber. Then they make changes themselves and send revised budget bills (usually in the form of substitute bills) to the chamber floors for additional modification and votes. Usually there are differences between the budget bills passed by the House and by the Senate. In these cases, the bills often are referred to a joint committee (called a conference committee) where differences can be resolved. Each chamber then must approve the conference committee’s report before sending the final legislation to the governor for a signature, veto or executive amendment. If the governor signs the budget bill into law, or if the Legislature overrides the governor’s veto, the bill becomes an act.

How could Alabama improve its budgeting process?

In 2014, the Center on Budget and Policy Priorities rated Alabama as “low” in using fiscal planning tools that could improve our budgeting process. While the analysis had some limits and the state has made some improvements since then, Alabama still fails to use many tools available in other states that could improve how we write our budgets. Some of the areas where Alabama could improve its budgeting process include:

- Forecast revenues into the future. Alabama passes a future budget based, in large part, on revenues collected during the current budget year. State leaders often have a good idea of what economic conditions and revenues may look like in the next year but have no formal process to forecast revenues for several years. A more deliberate approach involving outside experts could help Alabama plan for future budgets and needed revenue.

- Prepare fiscal notes with multiyear projections. Bills considered by the Legislature that will cost or save the state money must be accompanied by a fiscal note from the LSA describing the bill’s financial impact on the state. These fiscal notes, however, are often vague and limited in detail. More robust data would help lawmakers understand the financial implications of legislation they’re considering.

- Get a stronger current-year baseline on services. Alabama’s budgets are based in part on requests prepared by state agencies and submitted to the governor each fall. These plans, however, are not readily available to the public and often lack detailed analysis of the cost of existing and anticipated services. Stronger and more specific estimates of the cost to extend current services into future years would help the governor and Legislature determine future revenue needs. In addition, greater transparency would allow Alabamians adequate time to weigh in, strengthening elected officials’ ability to ensure they are adequately responding to and funding the needs of the people.

In 2014, the Center on Budget and Policy Priorities rated Alabama as “low” in using fiscal planning tools that could improve our budgeting process.

- Seek independent consensus revenue forecasts. The Executive Budget Office (EBO) prepares revenue forecasts for the governor, and the Legislative Services Agency’s Fiscal Division prepares them for the Legislature. In past years, these forecasts could diverge widely between the House and Senate. More recently, forecast differences between the LSA and EBO have been minor, and the two chambers generally agree on their revenue projections. But Alabama still should include outside, independent experts in their revenue estimates, such as experts from the state’s major universities. Including outside experts in the revenue forecasting process could make the process more objective and reduce politicization.

- Enhance fiscal flexibility through gradual earmarking reform. Make Alabama’s budget process more agile and responsive to the state’s evolving needs and priorities by pursuing a measured approach to earmarking reform. Policymakers should seek to strike a balance between preserving the benefits of earmarking and providing the state’s budget with necessary adaptability. This approach could include doing the following:

- Initiate a comprehensive review of Alabama’s existing earmarking practices. Identify programs and areas where earmarking can be gradually reduced or modified to allow for greater spending flexibility. This analysis should take into consideration both short-term budgetary requirements and long-term strategic goals.

- Consider a phased approach to earmarking reform. Begin by identifying non-essential or outdated earmarks that can be modified without requiring constitutional amendments. This approach would allow for incremental changes that could lead to a more flexible budget over time.

- Implement pilot projects to showcase the positive outcomes of earmarking reform in specific sectors. Highlighting the improved allocation efficiency, responsiveness to pressing issues and overall positive impact on the state’s well-being would be important steps toward broader reform.

The Alabama Tax and Budget Handbook

Alabama should reform its outdated, imbalanced tax system to help working people get ahead and to ensure adequate funding for vital services like education and health care,

Alabama should reform its outdated, imbalanced tax system to help working people get ahead and to ensure adequate funding for vital services like education and health care,