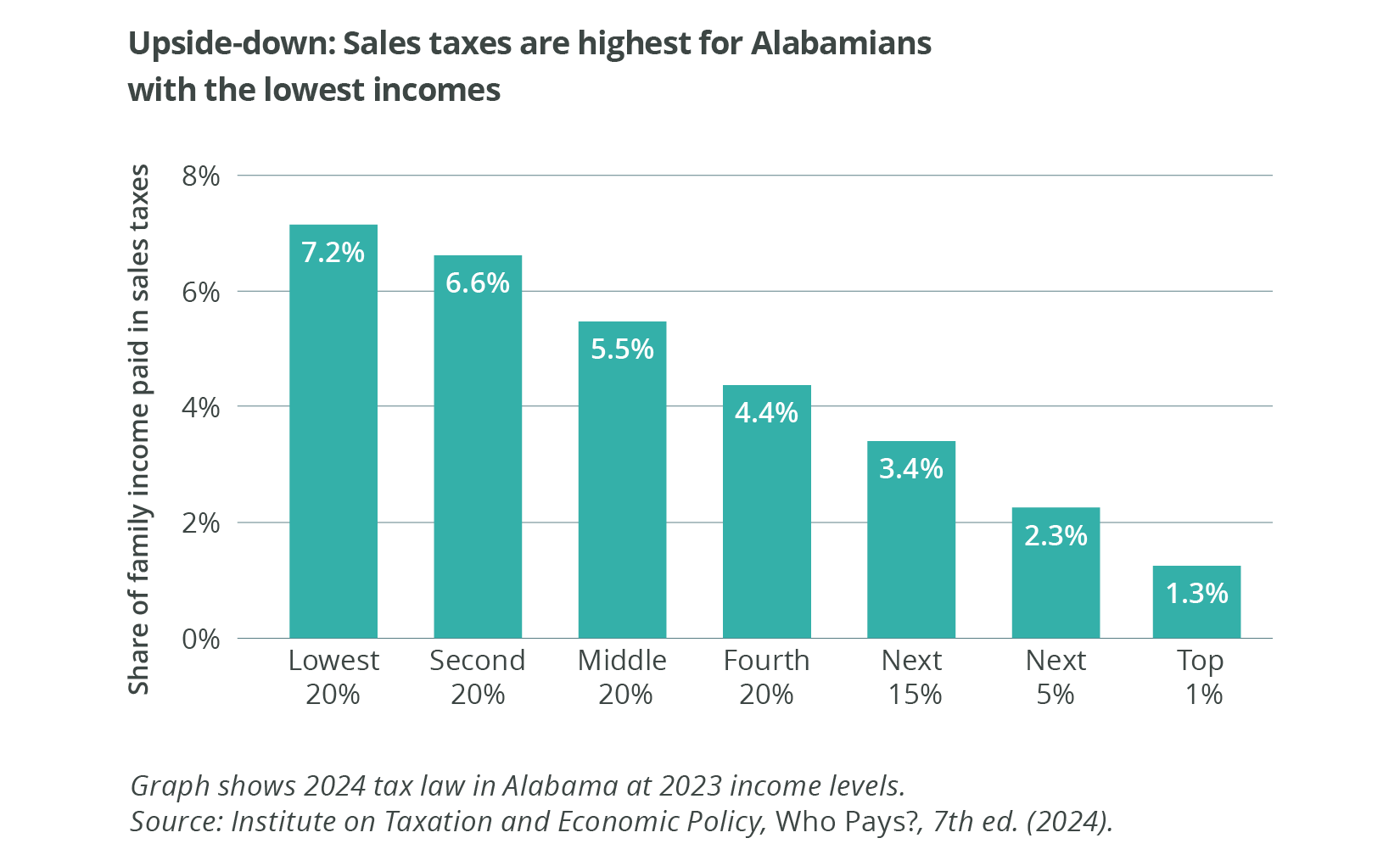

Feeling the pinch

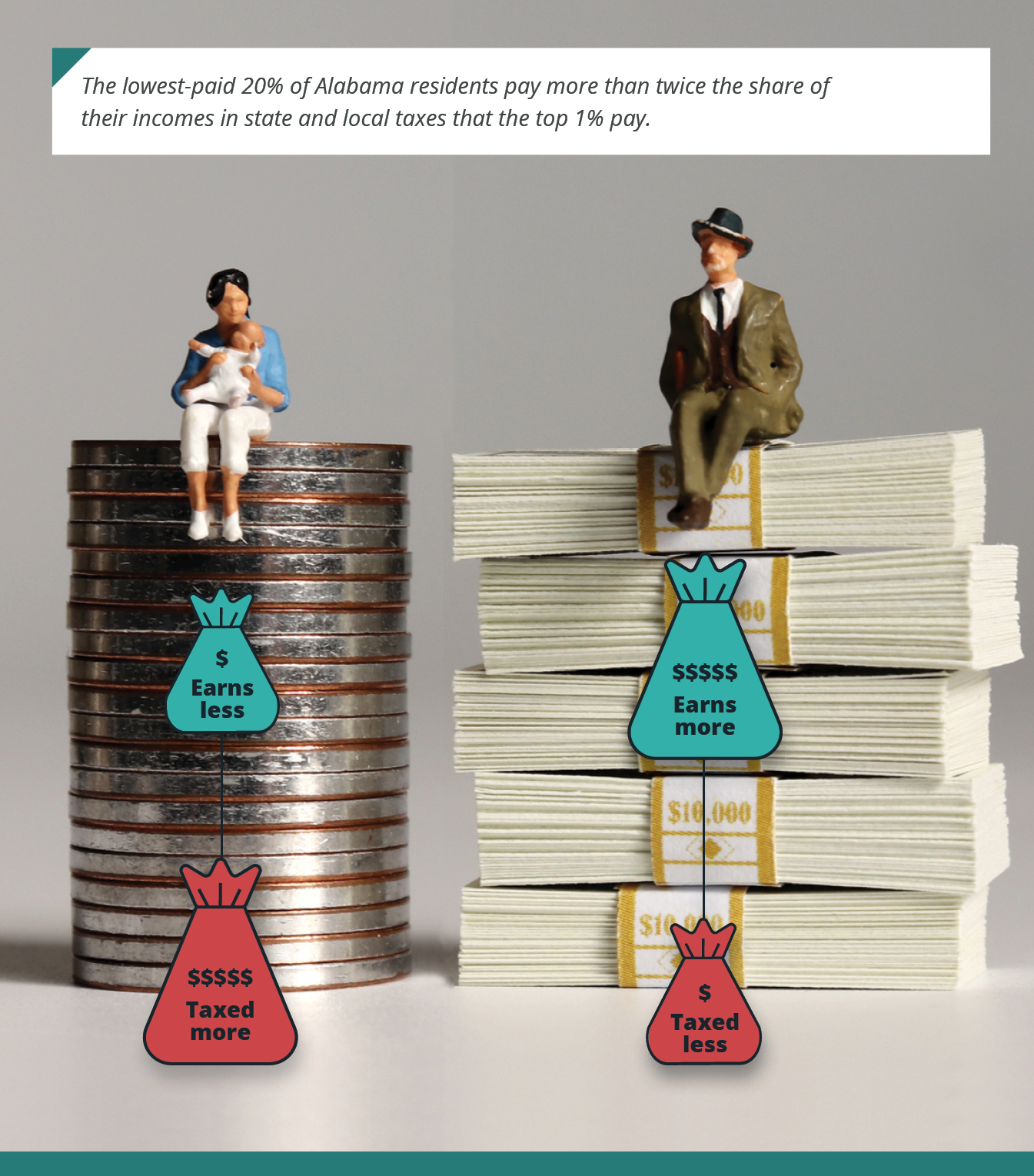

Alabama’s nearly flat income tax can’t offset our regressive sales taxes. As a result, the lowest-paid 20% of Alabama residents pay more than twice the share of their incomes in state and local taxes that the top 1% pay. It’s an upside-down tax system: It reduces the consumer spending that fuels economic growth and makes it harder for Alabamians with low and middle incomes to get ahead.

How does Alabama’s income tax work?

A 1933 amendment to the Alabama Constitution authorized the state to create a tax on personal income and set a limit of 5% for the tax rate. The Legislature enacted that tax in 1935, establishing three income tax rates for individuals that are still in place today:

- Yearly taxable income of up to $500 is taxed at 2%.

- Income from $501 to $3,000 is taxed at 4%.

- Income of $3,001 and above is taxed at the top rate, 5%.

Most states define their income tax by statute, meaning their legislatures can change it. But major parts of Alabama’s income tax are written into our constitution, which is much harder to change.

Ideally, an income tax should be the most progressive tax, because it’s the easiest one to structure to help offset regressive taxes. When it began in 1935, Alabama’s graduated system of income tax rates was very progressive. That year, when the state began taxing incomes of $3,600 or more for a family of four, teachers earned around $500. Only about 7,000 people (less than a quarter of 1% of the population then) earned enough to be taxed. But since then, the system hasn’t kept pace with inflation.

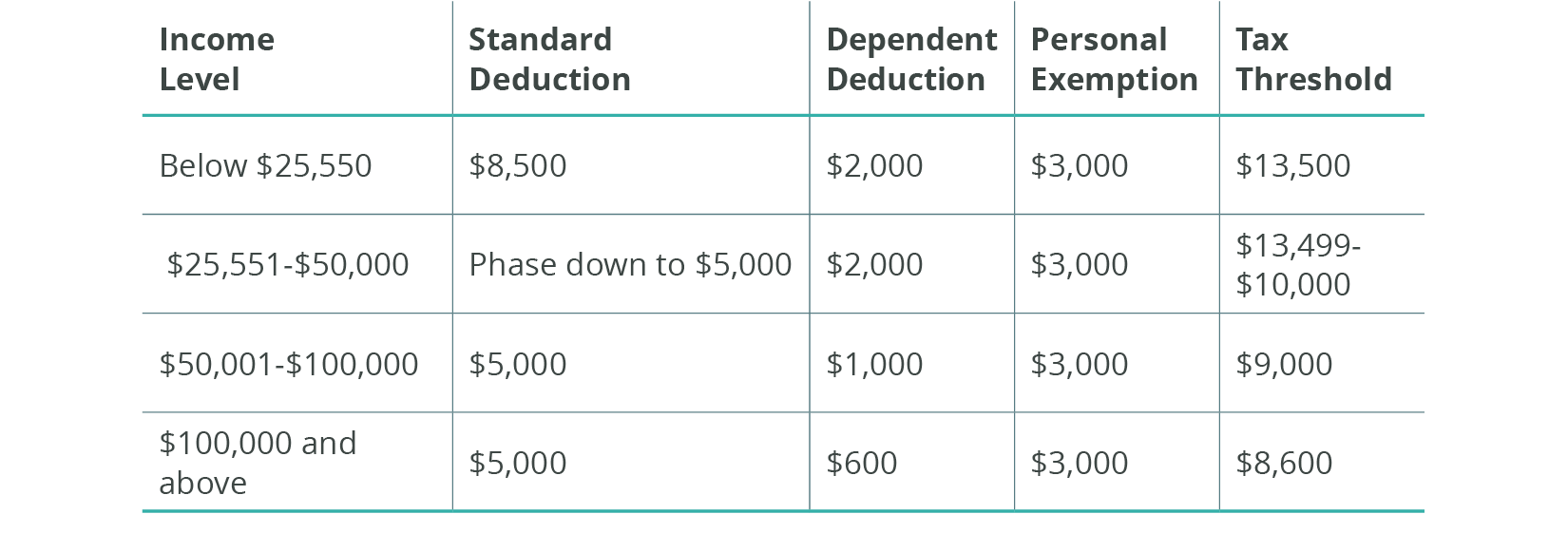

Like most states, Alabama uses exemptions and deductions to exclude everyone’s most basic costs of living from taxation. This is especially important to low-income taxpayers, for whom this small amount is a large share of income. But our exemptions and deductions are lower than in many other states.

The 1935 law set personal exemptions of $1,500 for single adults and $3,000 for married couples. It also set a dependent deduction that lawmakers increased in 2006 and again in 2022. The standard deduction, for taxpayers who don’t claim itemized deductions, was added in 1951 and has increased three times, most recently in 2022 when the standard deduction increased to $3,000 for single adults and $8,500 for couples. Taxpayers can itemize if their deductions exceed the standard deduction. (See the chart on below for Alabama’s deductions by income level.)

Better, but we still have work to do

In 2022, Alabama increased its income tax threshold – the income where one begins to pay income tax – from $12,500 to $13,500 for a family of four by expanding deductions. Even so, Alabama still taxes families with low incomes deeper into poverty.

Racial inequity at a glance

While Alabama’s income tax system appears essentially flat, Alabama doesn’t tax many sources of income received by wealthier (and disproportionately white) taxpayers. Many of these tax breaks are available to older adults no matter what their income or wealth.

Because of these tax breaks, many seniors with higher incomes pay less in income taxes than do younger, working families. The targeting of these special tax breaks also increases racial disparities because of demographics and historic inequities in wealth accumulation. As a result, white retirees have around seven times as much untaxed retirement wealth as do Black retirees.

Nearly all defined-benefit retirement income is exempt from Alabama income tax. This includes state retirement benefits for teachers and state employees, U.S. civil service retirement, judicial retirement, military retirement, federal government retirement, Social Security and some private retirement benefits. Alabama does not count inheritance as income and only counts the increased value of stocks and bonds when they are sold. These exemptions, along with the deduction for federal income taxes, allow many wealthy people in Alabama to pay much lower state income taxes than wage earners do. Because white people are much more likely to receive defined-benefit retirement benefits, own stocks and bonds, inherit wealth and pay higher federal income taxes, they are more likely to benefit from Alabama’s income tax structure than are Black people or people with lower incomes.

How does Alabama’s income tax measure up?

Most states have made sure that people below the federal poverty line don’t have to pay income taxes. Alabama begins taxing a two-parent family of four at an income of $13,500. It’s an improvement from the pre-2006 level (just $4,500), but it’s still less than half of poverty-line wages (about $31,800 in 2024). Alabama’s income tax threshold is one of the nation’s lowest.

By contrast, Mississippi doesn’t start taxing such a family until they make $19,600 per year, and Georgia doesn’t start until they make $32,000.

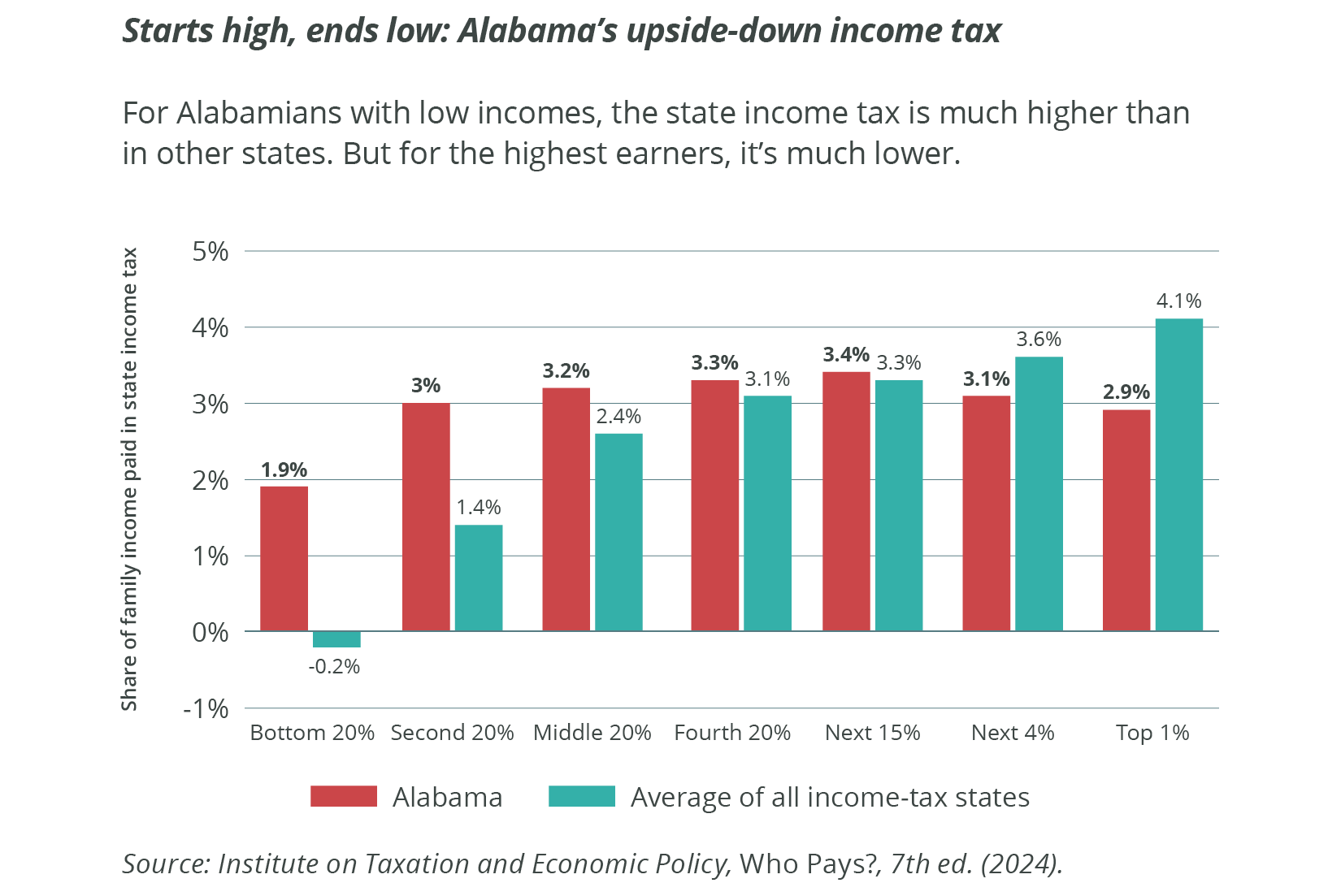

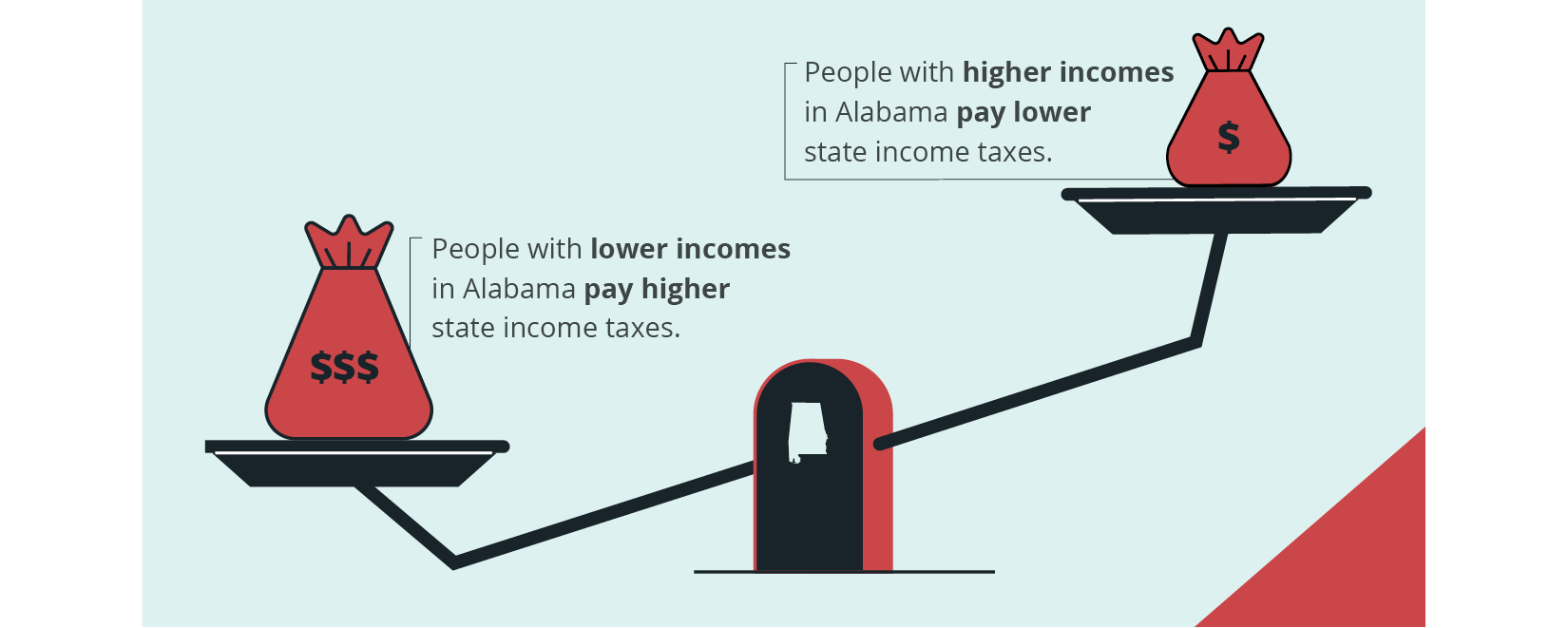

In Alabama, families with low and high incomes pay income taxes at the same rate: 5% on taxable income above $3,000. Most Alabama taxpayers pay at the top rate. In 2023, most of Alabama’s taxpayers paid around 3% of their income in state income taxes. Even the Alabama families with the lowest incomes pay 1.9% of their income. Nationally, many families with the lowest incomes pay less than 0% in state income taxes (depending on the availability of refundable tax credits), while the top 1% pay 4.1%. But in Alabama, the top 1% pay an average of 2.9% of their income in state income taxes, barely more than the 1.9% paid by taxpayers with the lowest incomes.

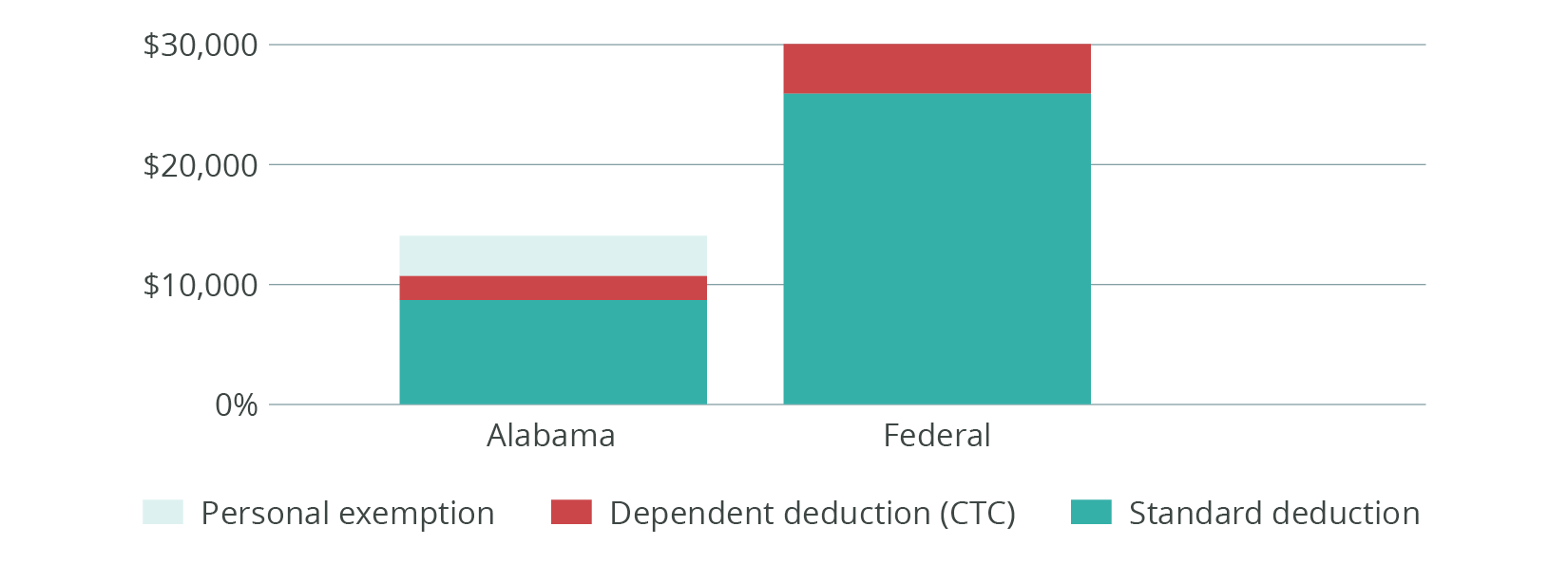

Anatomy of a tax threshold

The tax threshold – the income where one begins to pay income tax – is a sum of tax deductions and exemptions. Here’s how it worked when applied to 2022 Alabama and federal taxes for a two-parent household of four.

(In 2017, Congress ended the federal personal exemption, significantly increased the standard deduction and replaced the dependent deduction with an increased Child Tax Credit.)

Few other states impose an income tax nearly as high as Alabama does on a two-parent family of four at the poverty line. Alabama’s income tax on such a family in 2024 was $838. That family pays no federal income tax, and in most states would pay no state income tax at all.

Alabama’s income tax system is unfair for three reasons:

First are our out-of-date deductions. Despite an increase in 2022, our standard and dependent deductions are still below those in many other states. Alabama’s standard deduction for individuals ($3,000) is less than a quarter of the federal one; the maximum for couples ($8,500) is less than half. Alabama’s standard deduction is not tied to inflation, which means its value will continue to decline over time.

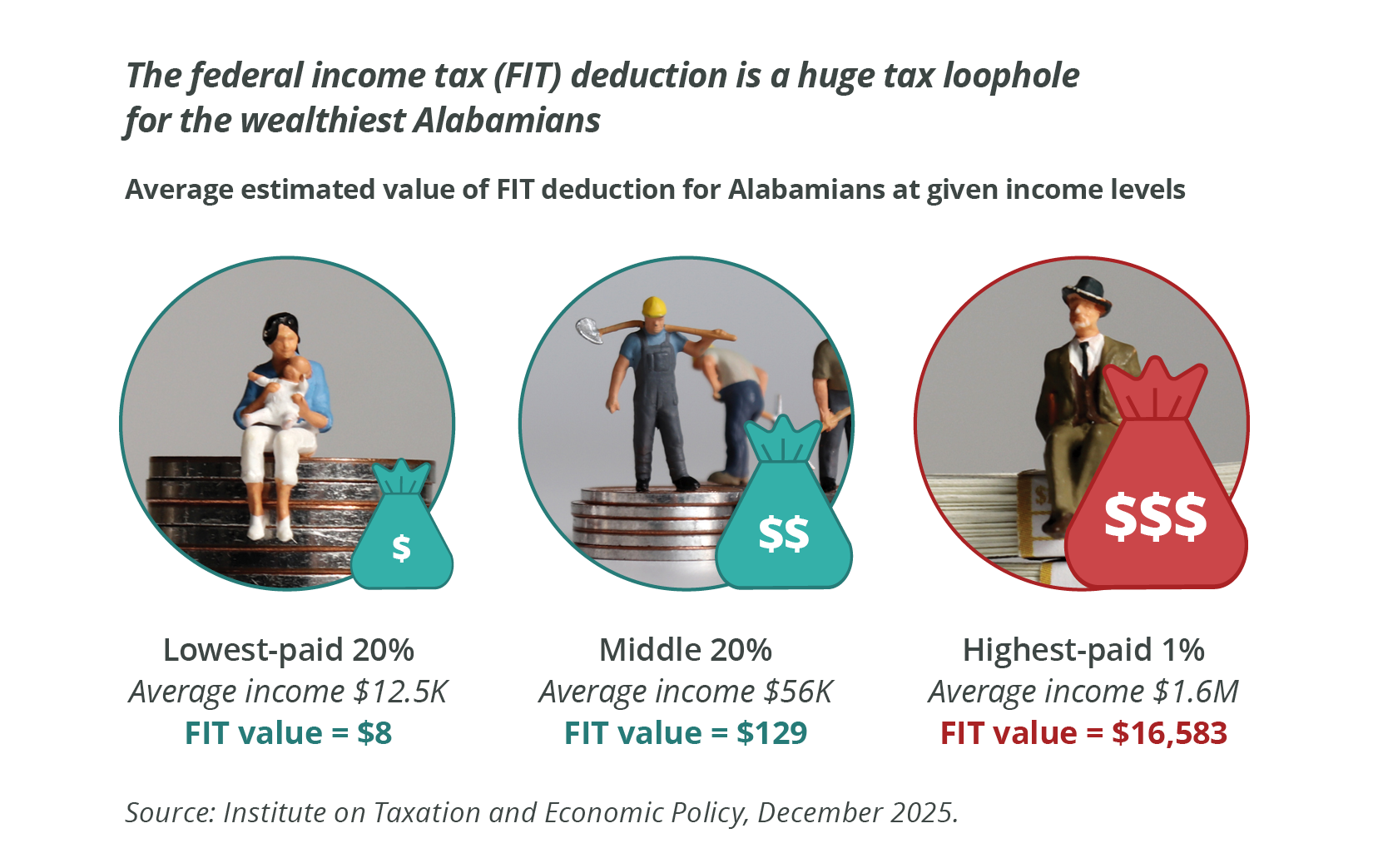

Second is a big tax break we give the highest earners. Alabama is the only state that allows taxpayers to deduct all of their federal income taxes before calculating their state taxes. A 1965 constitutional amendment entrenched this federal income tax (FIT) deduction. The FIT deduction gives higher-income earners a special break, because they can deduct more from their Alabama taxes than those who earn a lower income and pay less federal tax. Alabama forgoes about $1.26 billion of its potential income tax revenue because of this lopsided deduction, and 86% of the tax break’s value goes to the highest-paid 20% of taxpayers.

Third, Alabama also allows Social Security contributions to be deducted. In theory, this should help people with low incomes, who pay a higher share of their income toward Social Security. The catch is that the deduction is available only to those who itemize deductions, which excludes most people with low or middle incomes.

Unlike the federal government and many states, Alabama doesn’t give targeted tax breaks to people with less income. This is in contrast to the 31 states and the District of Columbia that have followed the federal example and created state-level Earned Income Tax Credits (EITCs), which allow many taxpayers with low incomes to receive a credit against taxes owed or a tax refund if they do not owe taxes. Alabama has not created an EITC, a failure that makes it harder for families with low incomes to get ahead and makes our income tax more unfair.

How could we improve our income tax?

Because much of Alabama’s income tax structure is spelled out in the constitution, changing it would require changing the constitution. If Alabama’s income tax more closely followed the system of exemptions and deductions used at the federal level and in many other states, working families would have more money available to spend. That would boost the economy and improve their quality of life. The following proposals would help modernize our income tax and make it fairer:

- Make income taxes less regressive and more progressive. Ensure people who make more money pay a larger share of their income in taxes than those who make less. Alabama’s state income tax rates top out at low income levels, making our income tax practically a flat tax. Transitioning to a more progressive system that requires households with higher incomes to pay a more equitable share of tax revenues would expand economic opportunity for families with lower and middle incomes. And it would make funding for vital public services more equitable and sustainable.

- Reform out-of-date deductions. Update Alabama’s standard and dependent deductions to align with modern economic realities and periodically adjust them for inflation to prevent their gradual erosion over time. This should include increasing the personal exemption and standard and dependent deductions. The state also should conduct a comparative analysis with deductions in other states to determine appropriate adjustments or link these dollar amounts to federal levels. These changes would allow Alabama’s deductions and exemptions to keep pace with increases in the cost of living.

- Eliminate the federal income tax (FIT) deduction. Repeal the provision that allows taxpayers to deduct federal income tax payments before calculating their state taxes. This lopsided deduction disproportionately benefits higher-income earners and results in a significant loss of revenue that could support public schools.

- Review Social Security contribution deductions. Examine the eligibility criteria for deducting Social Security contributions. Expand access to this deduction beyond itemizers to ensure it benefits a broader range of people with low and middle incomes. These changes would help ensure the deduction benefits those who need it most.

- Establish a state Earned Income Tax Credit (EITC). Introduce a state-level EITC program similar to the federal EITC and equal to at least 10% of the federal EITC amount. This credit would help low-paid working families make ends meet and help offset the regressive effects of Alabama’s high sales tax. This initiative also would provide a targeted reduction to lower-income taxpayers by allowing them to receive a credit against taxes owed or as a tax refund. Alabama can and should model this program after successful EITC programs in other Southern states like Louisiana, Oklahoma and Virginia.

- Gradually increase standard deductions. Phase in a plan that gradually increases standard deductions for individuals and couples. This would help rebalance Alabama’s upside-down tax system to be more equitable toward people with lower and moderate incomes. Policymakers also should enact higher-rate tax brackets for millionaires.