Alabama is making some big changes in the way Medicaid members get their care. Alabama Arise believes the new plans, if carried out well, will be a significant improvement over the current Medicaid system. One way to improve the chances for success is to have a strong consumer voice at the policy table.

The changes are happening on two tracks:

- Primary care for children, pregnant mothers and family planning.

- Long-term care for people who need assistance with activities of daily living.

Alabama Coordinated Health Networks (ACHNs) for primary care, maternity care and family planning

Under the new plan, seven regional Alabama Coordinated Health Networks (ACHNs) will coordinate primary care for Medicaid children, pregnant mothers and people who receive family planning services. Primary care includes well-child visits; EPSDT (Early Periodic Screening, Diagnosis and Treatment); adult screening, diagnosis and treatment; and preventive care. Each member will choose a primary care doctor to be their “patient-centered medical home.”

(Note: A “medical home” is not a live-in care facility, like a nursing home. It’s more like a “home base” you stay in touch with for all your health care needs.)

Your ACHN will have a phone line to call when a Medicaid member has a health problem. The basic idea is that nurses, social workers and care coordinators working with the primary care doctor can help people get the right care for the right problem without going straight to the emergency room (ER) whenever they get sick.

ER services are important when there’s a real emergency (like a broken bone, chest pains or other critical need). But they’re also very expensive. So going to the ER for routine problems like a sore throat or upset stomach is a drain on the Medicaid budget. And it’s not the best way to get the right care for ordinary health needs. Getting checked first by your primary care doctor or nurse leads to better care at lower cost.

The ACHN can help patients identify health goals, create a care plan and connect with community resources that promote better health. Another feature aimed at improving care is bonus payments for doctors who reach quality benchmarks.

The new ACHN plan will begin Oct. 1, 2019. It will serve about 750,000 Medicaid members across seven regions. Each ACHN will have a consumer representative on its board, as well as a Consumer Advisory Committee (CAC). Arise is working to recruit Medicaid members, parents and caregivers to serve in these important roles. We also are urging Medicaid to add a second consumer representative to each regional ACHN board.

Integrated Care Network (ICN) for long-term care

On the long-term care side, Medicaid already has started a new plan called the Integrated Care Network (ICN). The ICN coordinates care for Medicaid members who live in nursing homes or receive certain home- and community-based waiver services. There are only about 25,000 of these members across Alabama, so one statewide ICN serves all of them. Right now, about 70% of people served by the ICN live in nursing facilities, and 30% are living at home. The program’s goal is to help more people get long-term care services in their home and community, if that’s what they want. The ICN works with 13 Area Agencies on Aging across Alabama to coordinate long-term care for Medicaid members who qualify.

The ICN has a strong consumer voice at the policy table. Four consumer advocates serve on the governing board. And the Consumer Advisory Committee includes eight consumer representatives, including Alabama Arise, along with a long-term care doctor.

What triggered reform?

Since it began in 1970, Alabama Medicaid has operated on a fee-for-service basis, with patients seeking care on their own from providers who then bill Medicaid for services rendered. For healthy patients, such a system can provide sufficient care at a reasonable cost. But many Alabama Medicaid patients have complicated health problems, involving one or more chronic conditions that are difficult and expensive to treat. Care providers often have difficulty monitoring patient care over time and educating patients on prevention and healthier lifestyles.

As Medicaid costs rose with enrollment growth during the Great Recession of 2008, state officials began to consider program changes that would both control budget growth and improve health outcomes.

In 2011, a few regional pilot projects began providing care coordination for people with chronic conditions, such as diabetes, cancer or substance use disorder. These successful experiments laid the groundwork for the regional care organizations (RCOs) that the Legislature authorized in 2013. Under the RCO plan, Alabama offered care coordination to people with chronic conditions statewide. Technical delays and other problems led Gov. Kay Ivey to cancel the RCO plan shortly after she took office in 2017, but the care coordination system remained in place. This time around, Medicaid will expand it even further – to serve not just patients with chronic illness but the majority of Medicaid members.

Long-term care reform took a different but parallel path. Alabama has long relied mainly on nursing homes to provide Medicaid long-term care services, even though home- and community-based services are far less expensive. The aging of the Baby Boom generation poses big challenges for the old system. A surge in nursing home patients would strain state budgets, and a movement for greater patient choice is changing the long-term care business. Alabama’s ICN has the potential to become a national model for expanding options in long-term care.

Bottom line for members

- Regional ACHNs open Oct. 1, 2019. Through their primary care doctor, children, pregnant moms and family planning patients can get new services focused on prevention, care coordination and health improvement.

- The primary care doctor is the patient’s “medical home” – the first place to contact for ordinary health needs. The goal: Reserve ERs for true emergencies.

- A new focus on improving patient health gives doctors bonus payments for better outcomes. Special projects will target substance use disorders, infant mortality, and obesity and obesity prevention.

- The ICN now gives long-term care patients more coordination of services and more choice in their care setting.

- Consumer representatives give Medicaid members a new voice at the policy table.

Map of Medicaid ACHNs

Keywords in Medicaid reform

A basic understanding of these keywords will help Alabama Medicaid members navigate the changes that are underway and help advocates and others follow ongoing developments in the program:

ACHN (Alabama Coordinated Health Network) – beginning Oct. 1, 2019, any of seven regional organizations that administer Medicaid services for children, pregnant women and family planning patients in Alabama, with a special focus on care coordination to eliminate barriers to adequate health care.

Area Agency on Aging (AAA) – any of 13 regional offices that serve older Alabamians by coordinating state and federal services such as senior centers, Aging and Disability Resource Centers and the Alabama Cares caregiver support network. The AAAs provide case management for Medicaid long-term care in the home, community and nursing facilities through the new Integrated Care Network (ICN).

Care coordination – the practice of organizing patient care activities and sharing information among all parties concerned to achieve more effective and efficient care. Care coordination has a narrower focus than case management.

Case management – a collaborative process of assessment, planning, coordination and advocacy for options and services to meet a person’s health needs. Case management has a broader reach than care coordination, also addressing social determinants of health like housing, nutrition and transportation.

EPSDT (Early Periodic Screening, Diagnosis and Treatment) – comprehensive and preventive health services guaranteed for children under age 21 who are enrolled in Medicaid.

Home- and community-based services (HCBS) – Medicaid long-term care services for qualifying members who choose to live at home or in a community care setting. In Alabama, these services are delivered through seven waiver programs. Two of these – Elderly & Disabled (E&D) and Alabama Community Transition (ACT) – are part of the new Integrated Care Network.

ICN (Integrated Care Network) – Alabama Medicaid’s long-term care reform program promoting person-centered care in the least restrictive setting of the patient’s choice.

Long-term care – health care, personal care and social services provided to people with chronic illness or disability, either in institutional or home and community settings.

Medicaid – federal and state health insurance program for people with low incomes and few resources. Alabama Medicaid covers mainly children in families up to 146% of the federal poverty level (FPL), pregnant women up to 146% FPL, low-income people with disabilities, and low-income people in nursing homes. Parents are eligible in Alabama only if their income is 18% FPL or lower.

Medicaid member – any individual enrolled in a Medicaid program.

Patient-centered medical home – a health care setting that offers patients comprehensive, coordinated primary care; an ongoing relationship with a primary care doctor; and referrals for necessary additional care.

Preventive care – health care that emphasizes healthy behavior, regular testing and screening aimed at early detection and treatment.

Primary care – routine health care, including diagnostic, therapeutic and preventive services, as well as management of chronic conditions.

Waiver – permission granted by the federal government that allows the state to “waive” or change ordinary Medicaid rules to provide specific services to a targeted group, such as long-term care patients.

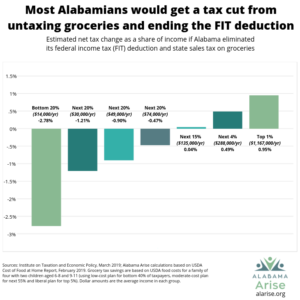

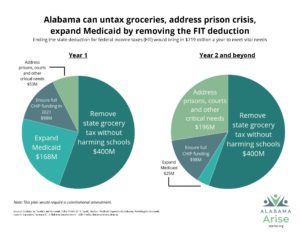

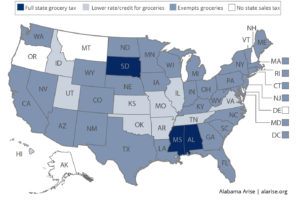

Sales taxes are especially regressive in Alabama, because they apply to many kinds of spending that are not optional.

Sales taxes are especially regressive in Alabama, because they apply to many kinds of spending that are not optional.